Buying a car is one of the biggest financial decisions you’ll make. Whether you’re considering a new versus used car, the choice affects your budget, lifestyle, and peace of mind for years to come.

At LifeEventGuide, we’ve helped countless people navigate this decision by breaking down what actually matters. This guide walks you through the financial realities, reliability factors, and personal priorities that should shape your choice.

Financial Considerations When Buying a Car

The Real Cost of Ownership

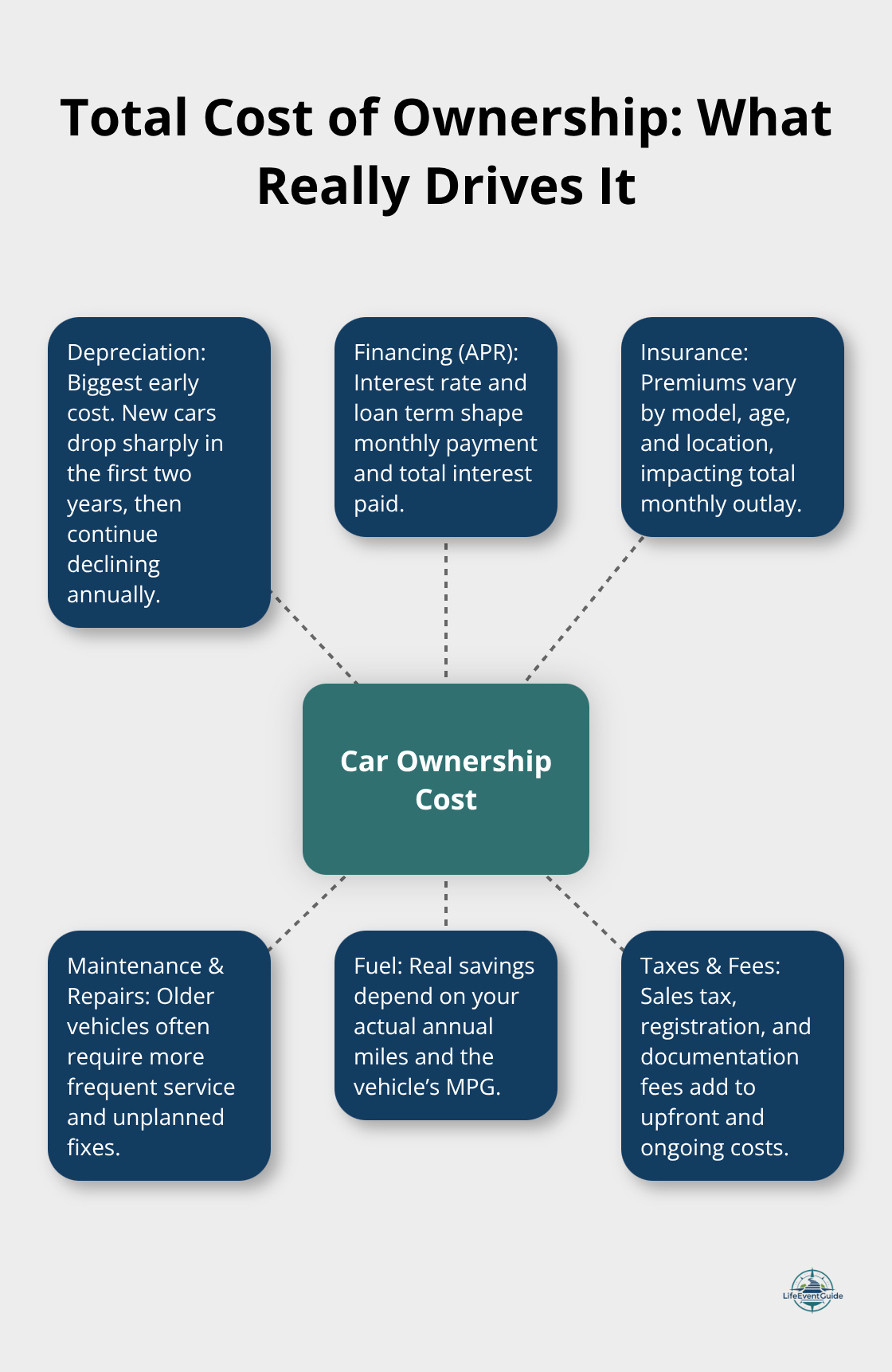

The sticker price tells only half the story. Experian data from Q3 2025 shows the average new car costs about $748 monthly versus $532 for used cars, but this masks a more complex financial picture. A new 2023 Kia Sorento at $32,000 looks expensive next to a used 2020 model at $24,000, yet the $8,000 difference shrinks when you factor in what actually happens over time. New cars depreciate about 30% over the first 2 years, then continue to depreciate 8-12% each year after that. Used cars have already absorbed much of that initial hit, which is why a low-mileage used vehicle often delivers stronger value retention relative to its purchase price. The financing gap matters too: new-car loans averaged 6.56 percent APR in Q3 2025, while used-car loans sat at 11.40 percent.

If you finance a $24,000 used car at that higher rate over 67 months versus a $32,000 new car at the lower rate over 69 months, the monthly payment difference narrows considerably, and sometimes the new car becomes the cheaper monthly option. Comparing total costs matters far more than comparing purchase prices alone.

What Maintenance Actually Costs

Used cars demand more attention to your wallet. A 13-year-old car with 100,000 miles typically costs around $2,000 annually in maintenance-roughly $170 per month. Over a 10-year ownership period, that adds up to approximately $20,000 in repairs and upkeep. New cars come with full manufacturer warranties, commonly covering 3 years or 36,000 miles, which eliminates most early maintenance expenses. Used cars may have no warranty at all, though certified pre-owned vehicles often include manufacturer-backed coverage that provides genuine peace of mind. Insurance premiums also diverge: new cars cost more to insure due to higher replacement costs, though the difference varies by model and your location. The real decision hinges on whether you’re comfortable absorbing unexpected repair bills or prefer the predictability of a warranty.

Getting the Numbers Right

Obtain quotes from your insurance provider for both options before you decide, as this cost can swing your total ownership calculation significantly. For used cars, always pull a vehicle history report and consider paying for an independent inspection before purchase. These steps cost $150 to $300 upfront but prevent you from buying a car with hidden problems that could drain your budget within months. When you compare total loan costs, factor in insurance, maintenance, fuel, and taxes alongside the monthly payment. Tools like NerdWallet’s Total Car Cost Calculator help you see the full picture across a 5- to 10-year horizon. Pre-qualify for auto loans before you shop so you understand what interest rates you’ll actually receive. This knowledge shifts the negotiation in your favor and reveals whether a new or used car truly fits your financial situation.

Reliability, Warranty, and Peace of Mind

New Car Warranties Protect You When You Need It Most

New car warranties shield you from repair costs during the years when problems are least likely to occur. Most manufacturers cover 3 years or 36,000 miles as standard, with some brands extending to 5 years or 60,000 miles. This warranty covers parts and labor, meaning a transmission failure or engine defect costs you nothing. The real value isn’t just financial-it’s the certainty that you won’t face a $3,000 repair bill in year two. However, warranties expire precisely when older cars tend to need them most. Once you hit that 36,000-mile mark, you’re on your own.

Used Cars and the Certified Pre-Owned Advantage

A used car arrives with its warranty already consumed or significantly depleted. Certified pre-owned vehicles bridge this gap by including a manufacturer-backed warranty. This matters because you essentially buy a new car’s warranty protection at a used car’s price. For non-certified used cars, you get nothing unless the previous owner transferred any remaining factory coverage, which is rare. This is why a $24,000 used 2020 Kia Sorento with 29,000 miles and a clean service history appeals to many buyers-the car is still young enough that major failures are uncommon, and you’ve already avoided the steepest depreciation cliff.

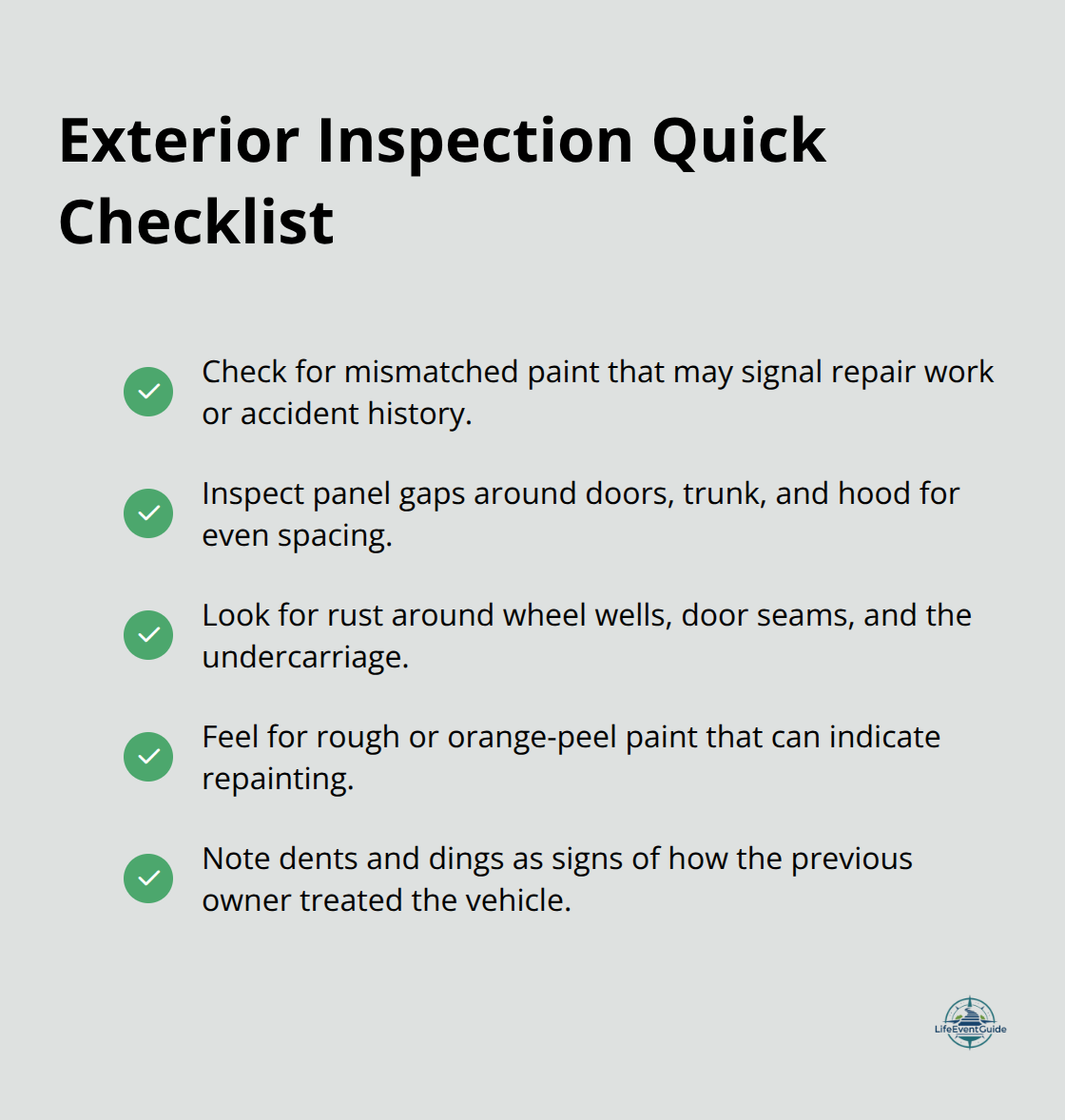

Vehicle History Reports and Independent Inspections Reveal Hidden Problems

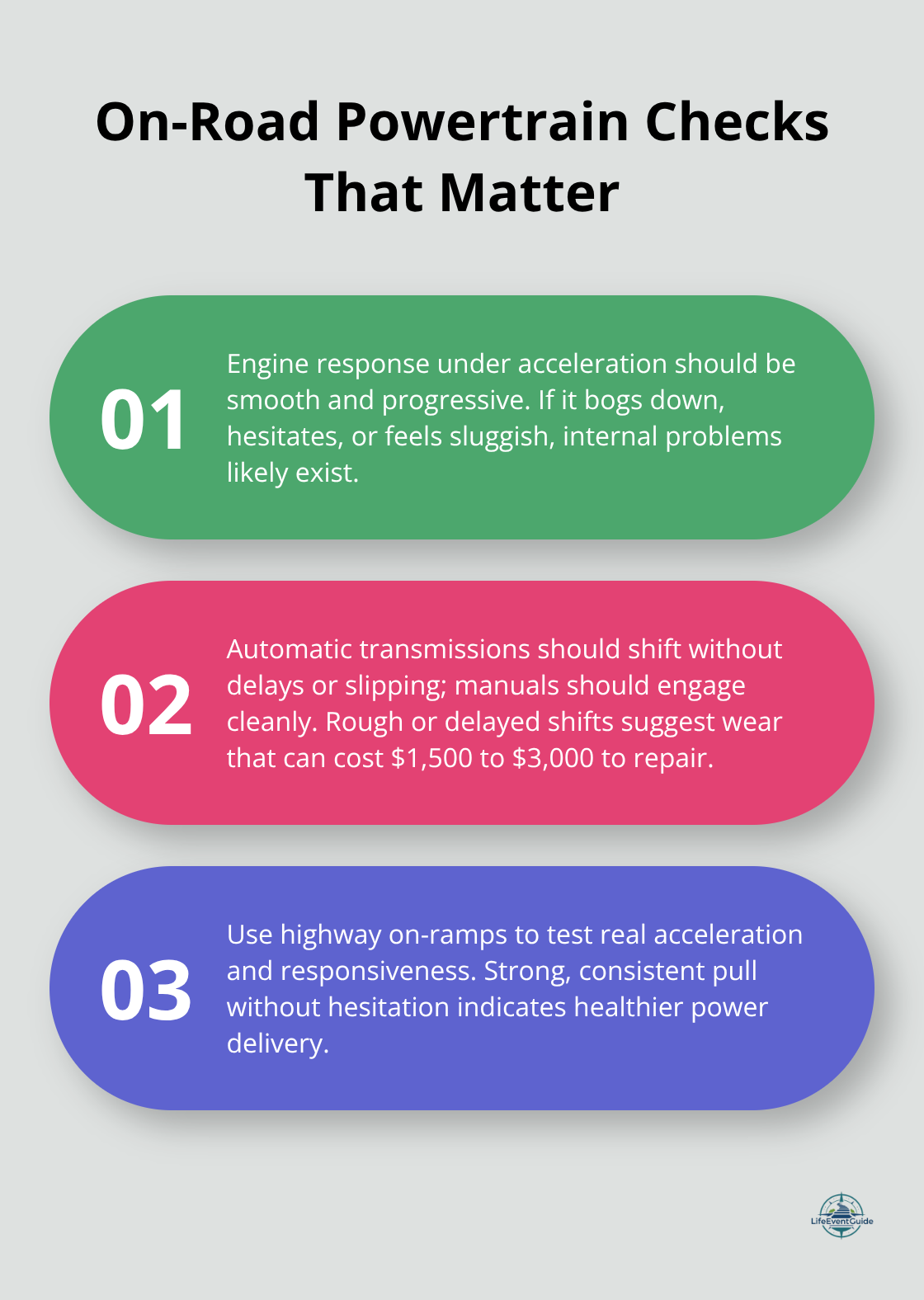

Vehicle history reports and independent inspections are your only defense against purchasing someone else’s problems. Services like Carfax or AutoCheck reveal accident history, title status, service records, and odometer readings. An independent pre-purchase inspection by a trusted mechanic costs $150 to $300 but catches hidden damage that no report reveals. This inspection should verify that the seller’s name on the title matches their driver’s license-a critical step that prevents fraud from curbsiders who flip cars without legal ownership. Mechanics check suspension wear, transmission responsiveness, brake condition, fluid leaks, and rust patterns that predict future failures.

Maintenance History Determines How Long Your Car Lasts

For a used car, a thorough inspection is non-negotiable. A 13-year-old car with 100,000 miles will cost around $2,000 annually in maintenance, but a thorough inspection identifies whether this particular car will land at $1,500 or $3,000. Expected lifespan depends entirely on maintenance history. A used car with documented regular oil changes and brake maintenance will last far longer than one with spotty records. Modern cars routinely reach 200,000 miles with proper care, but skipped services compound into expensive failures. When you compare a new car’s predictable costs against a used car’s variable repair landscape, the inspection transforms guesswork into informed decision-making. This foundation of knowledge about your vehicle’s actual condition sets the stage for understanding how lifestyle factors and personal priorities shape the final choice between new and used.

How Your Driving Patterns Shape the New Versus Used Decision

Annual Mileage Determines Fuel Economy’s Real Value

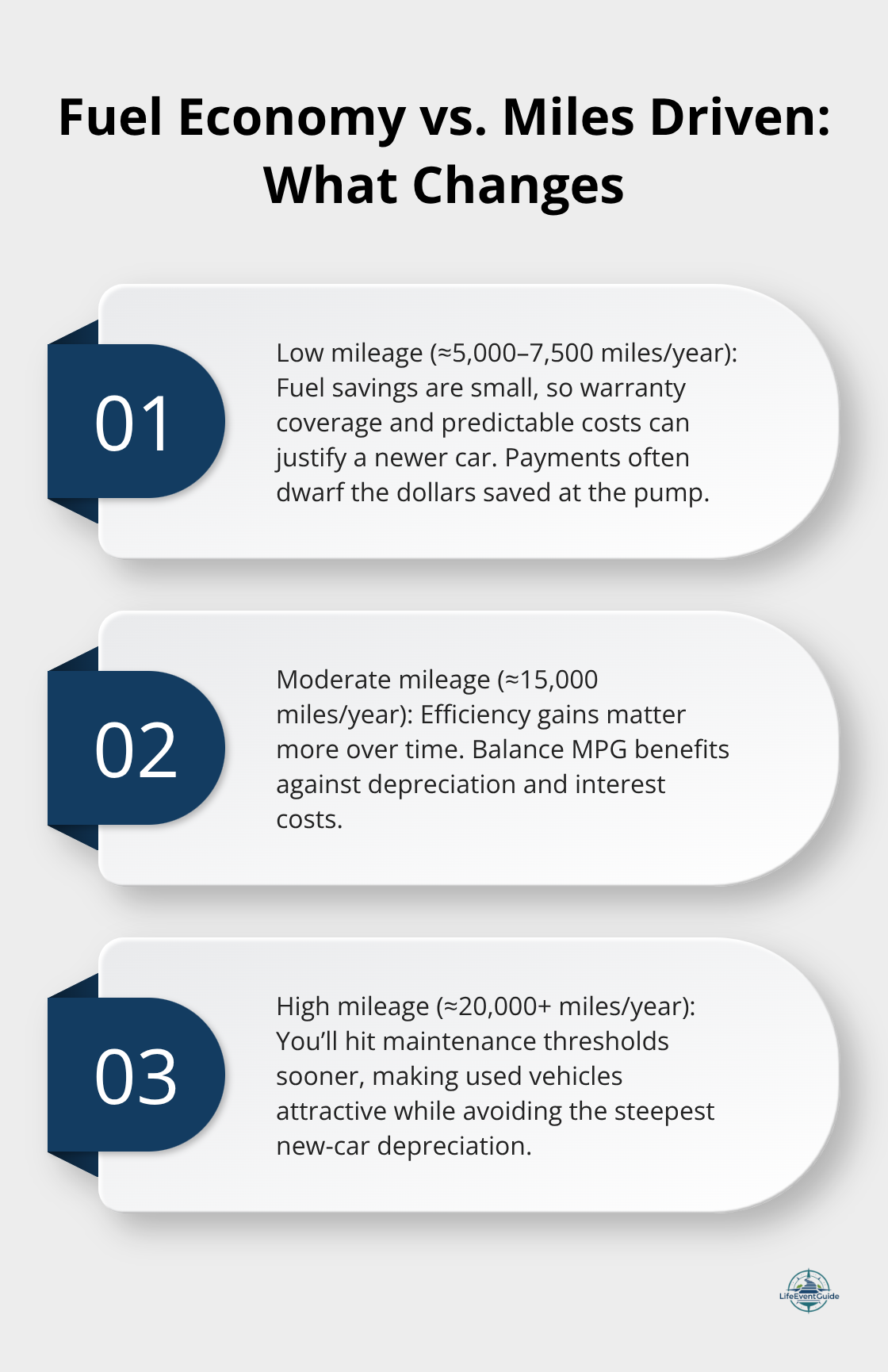

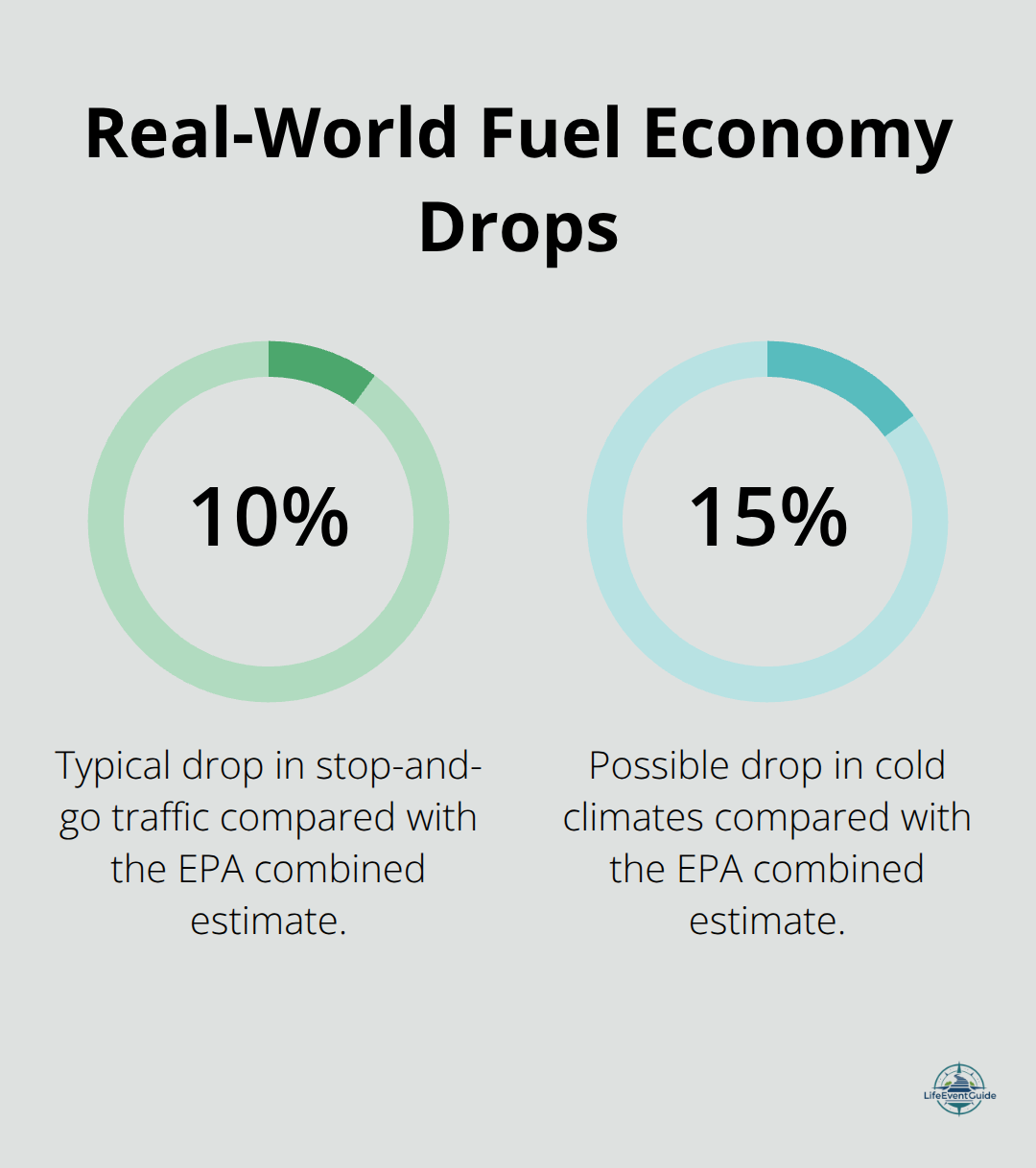

Your annual mileage transforms fuel efficiency from a marketing talking point into actual dollars. If you drive 7,500 miles yearly, a newer car’s superior fuel economy becomes almost irrelevant financially. A 2010 model at 40 miles per gallon consumes roughly 188 gallons annually, costing around $752 per year at current fuel prices. A 2023 model at 50 miles per gallon uses about 150 gallons, saving you approximately $150 annually or $1,500 over a decade. That $1,500 fuel savings vanishes in a single month of higher payments on a new car.

However, if you drive 15,000 miles yearly, fuel efficiency gains double, making the newer car’s economy genuinely meaningful over time. The critical calculation involves comparing your actual annual miles against the car’s depreciation curve and financing costs. A high-mileage driver racking up 20,000 miles yearly should lean toward used vehicles because you’ll hit major maintenance thresholds faster anyway, so you might as well avoid the steepest depreciation hit. Low-mileage drivers who put 5,000 miles annually on their car face the opposite reality: a new vehicle’s warranty and lower maintenance costs justify the premium because you’ll own the car through its warranty period without heavy use.

Driving Habits Affect Reliability and Risk

Driving habits matter equally to annual mileage. If you take frequent long highway trips, a newer car’s reliability and updated safety features become genuine assets. City driving with stop-and-go traffic stresses brakes and transmissions harder, making a used car’s unknown maintenance history riskier. Off-road or unpaved-road driving demands a vehicle with known suspension integrity, which an inspection on a used car can verify but a new car guarantees through warranty coverage.

Technology and Features Shape Daily Experience

New cars offer the latest infotainment systems, driver-assistance features, and safety sensors that genuinely improve daily driving and resale appeal. A 2023 Kia Sorento includes adaptive cruise control, lane-keeping assist, and smartphone integration that a 2020 model may lack entirely. These features aren’t luxuries for families with young children or aging parents; they reduce accident risk and driver fatigue on long trips. However, a three-year-old used car still has modern technology without the $8,000 premium for the absolute latest version.

Environmental Impact Favors Used Cars in Most Scenarios

Fuel efficiency improvements matter less than many assume. The jump from 40 to 50 miles per gallon sounds dramatic until you calculate actual dollars. At $150 yearly savings, you’d need to own the car for 50 years to recoup an $8,000 premium through fuel alone. Environmental impact from manufacturing a new car also weighs against fuel savings for the first several years of ownership. A used car’s smaller environmental footprint from avoided production makes it the greener choice unless you keep the new car for 10+ years and drive it extensively.

Match Your Choice to Your Actual Driving Life

Try a new car for its warranty, latest technology, and guaranteed reliability if you plan to keep it beyond 100,000 miles and drive it frequently. Try a used car if you drive moderately, can afford an inspection, and accept variable maintenance costs in exchange for lower upfront payments and depreciation protection.

Final Thoughts

The new versus used car decision rests on three interconnected factors: your financial situation, your tolerance for maintenance uncertainty, and how you actually use your vehicle. New cars offer predictable costs through warranties, latest safety features, and lower maintenance expenses during ownership. Used cars deliver immediate depreciation protection and lower monthly payments, though they demand more attention to inspection and repair budgeting. Neither choice is universally right or wrong-the correct answer depends entirely on your circumstances.

Start with a total cost of ownership calculation across five to ten years, not just the monthly payment. Factor in insurance quotes, expected maintenance based on the specific model’s reliability history, fuel costs aligned with your actual annual mileage, and taxes. This complete picture reveals whether the $8,000 premium for a new car costs more or less than financing a used vehicle at higher interest rates while absorbing repair expenses. Pre-qualify for loans before shopping so you understand the interest rates available to you, then compare those rates across new and used options to make an informed new versus used car decision.

Write a pros-and-cons list specific to your priorities and gather competing price quotes from multiple dealers. Compare loan offers side by side, verify vehicle history reports before committing, and use our structured decision-making framework to transform this stressful choice into a manageable process where you control the outcome. This methodical approach prevents costly mistakes and builds confidence in your final decision.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.

Buying your first home is one of the biggest decisions you’ll make. Understanding the home buying timeline helps you stay organized and avoid surprises along the way.

At LifeEventGuide, we’ve created this step-by-step schedule to walk you through each phase. From preparing your finances to signing the final papers, you’ll know exactly what to expect.

Preparing Your Finances for Home Buying

The first step toward homeownership requires an honest look at your financial health. Your credit score determines everything in the mortgage process-lenders use it to decide whether to approve you and what interest rate you’ll pay. A score of 620 is the minimum for most conventional loans, but scores above 740 typically qualify for the best rates. If your score falls below 620, you need to improve it before applying. Check your credit report for errors at the authorized free source, annualcreditreport.com. Dispute any inaccuracies immediately because fixing them takes time. Pay down existing debts, especially credit card balances, since high utilization ratios damage your score. Avoid opening new credit accounts or missing payments for at least six months before applying for a mortgage-this period matters more than most people realize.

Calculate Your Down Payment and Closing Costs

Down payments range from 3% to 20% of the home price, depending on the loan type. Federal Housing Administration loans require only 3.5% down, while conventional loans typically need 5% to 20%. A 3% down payment on a $350,000 home means saving $10,500, but closing costs add another 2% to 5% of the purchase price-typically $7,000 to $17,500 for that same home. Many first-time buyers underestimate closing costs, which include appraisal fees, title insurance, inspection fees, and lender fees. You cannot borrow closing costs from your lender, so this money must come from your savings. Start saving now, and consider opening a high-yield savings account to grow your down payment faster than a traditional savings account.

Secure Pre-Approval Before House Hunting

Pre-approval for a mortgage changes everything before you start house hunting. Pre-approval means a lender has verified your income, debts, and credit, then committed to lending you a specific amount. This letter proves to sellers that you’re a serious buyer and can actually afford an offer. The process takes three to five business days and costs nothing. You’ll need recent pay stubs, tax returns from the last two years, bank statements, and a list of debts. Pre-approval differs from pre-qualification, which is just a rough estimate based on information you provide-it carries no weight with sellers. With pre-approval in hand, you move into the next phase ready to search for properties with confidence.

Finding Properties, Making Offers, and Inspecting Your Home

Work with a Real Estate Agent to Find Properties

With pre-approval in hand, you’re ready to search for properties. Most first-time buyers work with a real estate agent, and this choice matters significantly. Agents have access to the Multiple Listing Service, which shows all available properties in your area before they hit public websites. When selecting an agent, interview at least three candidates and ask about their experience with first-time buyers specifically. An agent familiar with your local market knows neighborhood trends, school district boundaries, and which properties tend to appreciate.

Stay Disciplined During Your Property Search

Once you start viewing homes, stay disciplined about your budget and must-have features. It’s easy to fall in love with a home outside your price range, but doing so creates financial stress immediately. Attend open houses on weekends when possible, as they draw multiple buyers and give you a sense of market competition. This exposure helps you understand what your money actually buys in your area and prevents emotional decisions later.

Make Your Offer and Negotiate Terms

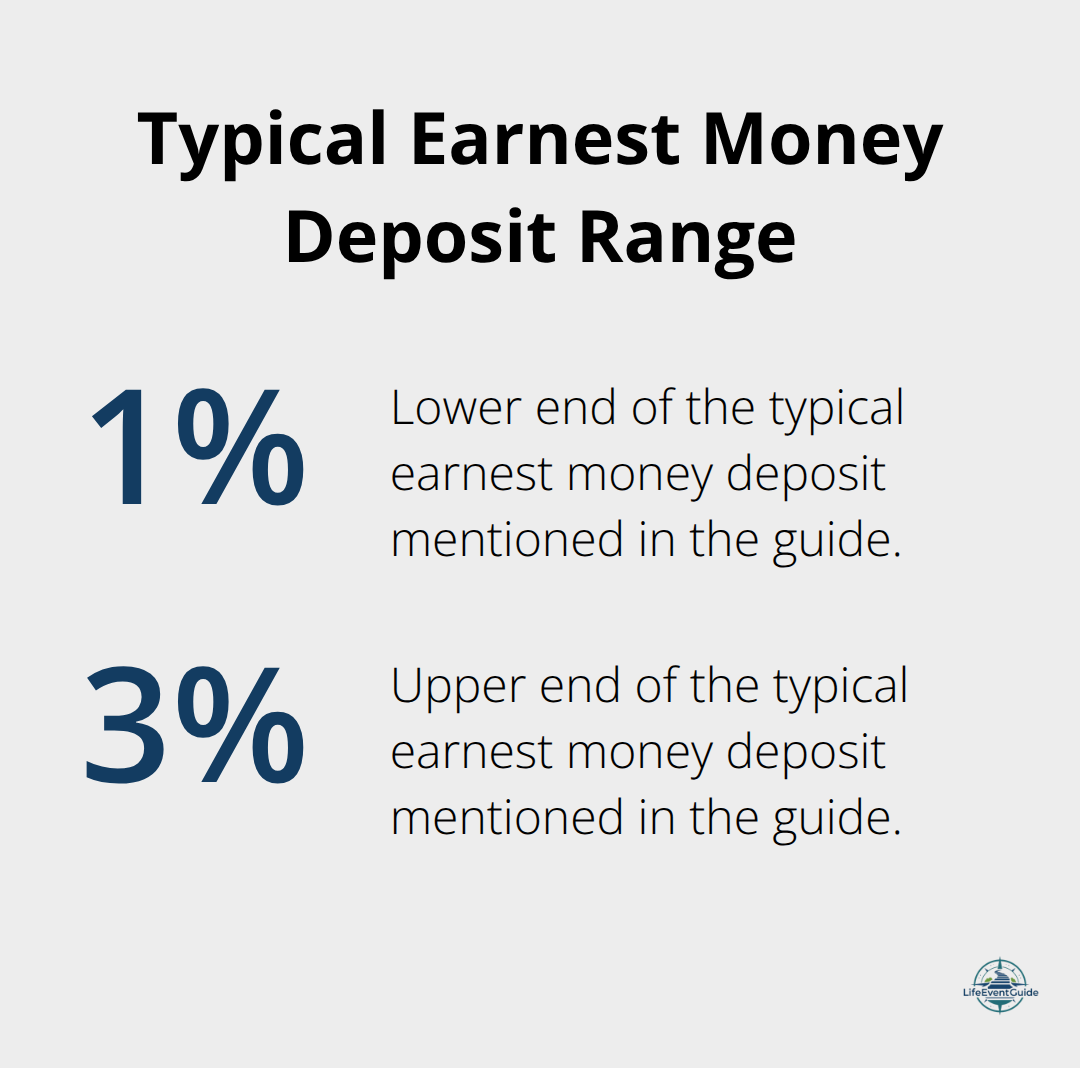

When you find a property you want, your agent will help you craft an offer. The offer includes the purchase price, earnest money deposit (typically 1-3% of the purchase price), and contingencies like inspection and appraisal. In competitive markets, offering above asking price or waiving contingencies might seem necessary, but this strategy backfires frequently.

Contingencies protect your interests without preventing sales in normal conditions.

Complete the Home Inspection

Once your offer is accepted, the inspection phase begins within 7-10 days. A professional home inspector examines the roof, foundation, plumbing, electrical systems, HVAC, and structural integrity, then provides a detailed report. This inspection protects you from inheriting expensive repairs-a roof replacement costs $8,000-$15,000 on average, while foundation repairs can exceed $20,000. If the inspection reveals significant issues, you can renegotiate the price, request repairs, or walk away entirely.

Verify the Appraisal and Protect Your Finances

Simultaneously, the lender orders an appraisal to verify the home’s value matches your offer price. The appraisal typically takes 7-10 business days and costs $400-$600. If the appraisal comes in lower than your offer price, you have three options: negotiate a lower price with the seller, increase your down payment to cover the gap, or withdraw your offer. This step stops many buyers from overpaying in heated markets. Throughout this phase, communicate with your lender about any changes to your finances-new debts, job changes, or large purchases can jeopardize your approval. Stay disciplined during this waiting period, and avoid making major financial moves until closing. Once the inspection and appraisal clear, you move into the final phase where you’ll review loan documents, conduct a final walkthrough, and prepare to sign the papers that make you a homeowner.

What Happens in Your Final Week Before Closing

Review Your Closing Disclosure Carefully

The three weeks between appraisal approval and closing move quickly, and most first-time buyers feel overwhelmed by paperwork during this stretch. Your lender will send you a Closing Disclosure, a standardized document required by federal law that outlines your final loan terms, interest rate, monthly payment, and all closing costs broken down by line item. You must receive this document at least three business days before closing, and you should read it carefully against your initial Loan Estimate to spot any changes. Common discrepancies include title insurance costs that shifted, property taxes recalculated based on new assessment data, or lender fees that increased without explanation. If anything differs significantly from your Loan Estimate, contact your lender immediately and ask for a written explanation before closing day arrives. Many lenders add unnecessary fees or miscalculate property taxes, so questioning these items protects your wallet.

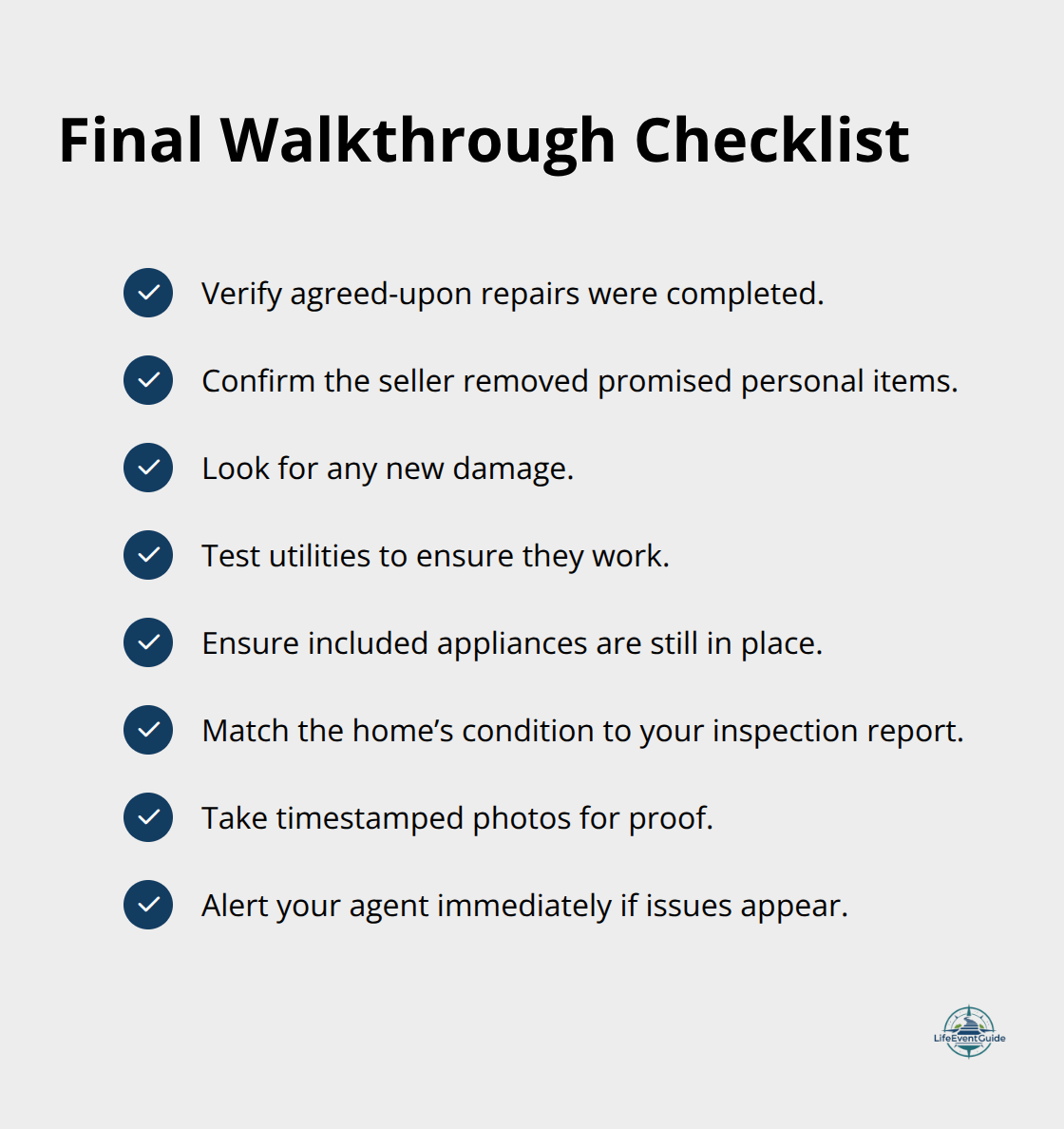

Conduct Your Final Walkthrough

Schedule your final walkthrough 24 hours before closing, not three days before, because things change in real estate constantly. Bring a checklist and verify that agreed-upon repairs were actually completed, that the seller removed personal items they promised to take, and that no new damage appeared. Check that utilities still function, appliances included in the sale remain in place, and the property matches the condition documented during your inspection.

Take photos of the final walkthrough as proof of the property’s condition on closing day. If the seller failed to complete promised repairs or removed items you expected, document everything and notify your real estate agent immediately so they can contact the seller’s agent before closing.

Prepare for Closing Day

Closing day itself involves signing approximately 50 to 100 pages of documents, though many are duplicates required by different lenders or government agencies. Arrive 15 minutes early, bring a government-issued ID and proof of homeowners insurance, and plan to spend 60 to 90 minutes at the title company or attorney’s office. The closing agent will walk you through each document, but they cannot provide legal advice, so if anything confuses you, ask questions directly. Wire your down payment and closing costs to the title company before closing day, never the day of closing, because wire fraud targeting homebuyers costs victims significant losses per incident. Contact your lender directly using a phone number from their official website to confirm wire instructions rather than trusting email or documents provided by the title company (this step prevents criminals from intercepting your funds through fraudulent communications).

Complete the Final Transfer

After all documents are signed and funds transfer, the title company records the deed with the local government, and you officially own the property. Your lender will fund the mortgage and send the seller’s proceeds, typically completing within 24 hours. Keep copies of every document you sign at closing, including the final Closing Disclosure, deed, title insurance policy, and mortgage note, because you’ll need these for tax purposes, future refinancing, or if disputes arise later.

Final Thoughts

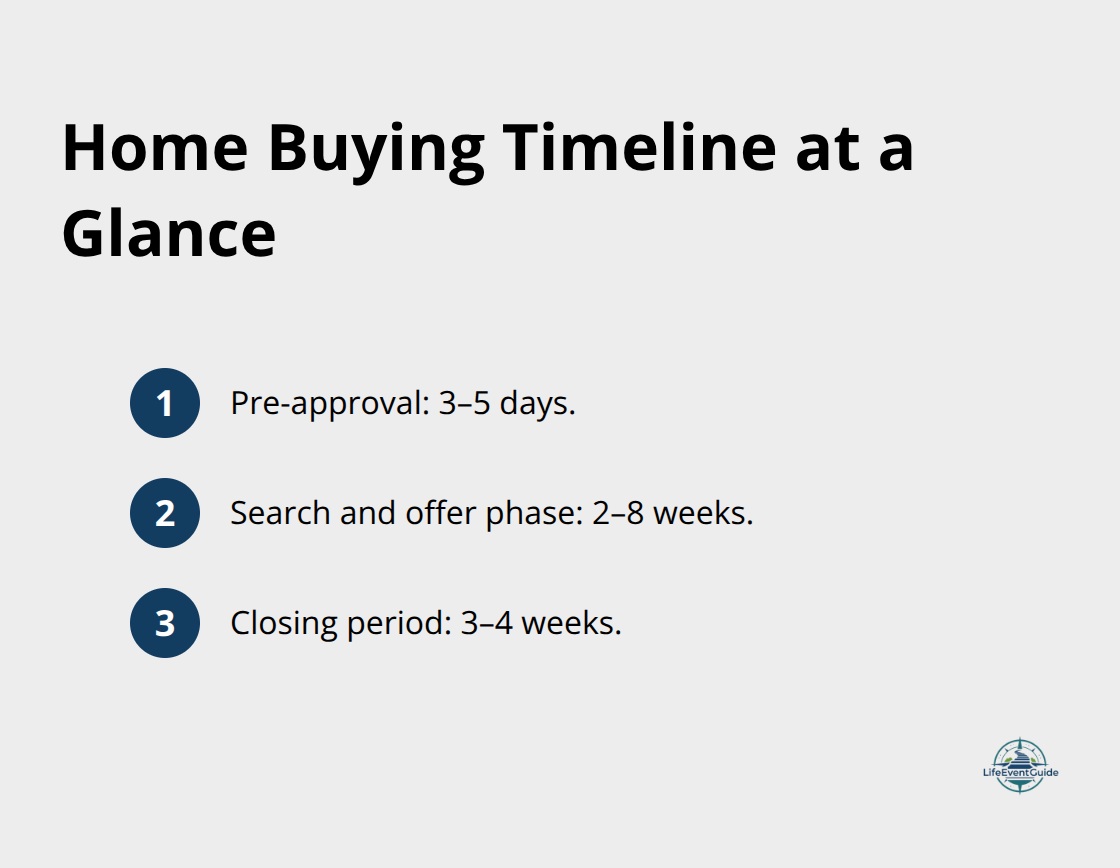

You’ve now walked through the entire home buying timeline from financial preparation through closing day. The journey involves multiple phases, each with specific tasks and timelines that compound if you skip steps or rush through them. Pre-approval takes three to five days, the search and offer phase typically spans two to eight weeks depending on market conditions, and closing takes another three to four weeks after your offer is accepted. Understanding this schedule prevents panic when timelines stretch longer than expected.

First-time buyers commonly make preventable mistakes that cost thousands of dollars or derail purchases entirely. Overextending your budget happens when you fall emotionally attached to a property and ignore your pre-approval limits. Opening new credit accounts or making large purchases between pre-approval and closing jeopardizes your loan approval, even after you’ve been cleared to proceed. Skipping the home inspection to save $300–$500 exposes you to repair costs that dwarf inspection fees, while waiving contingencies in competitive markets removes your protection if the appraisal comes in low or inspections reveal major problems.

Moving into your new home marks the beginning of homeownership, not the end of planning. You’ll face decisions about maintenance schedules, property taxes, homeowners insurance adjustments, and long-term improvements. Visit our publisher recommendations to explore resources that support your transition into homeownership with confidence and clarity.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.

Bringing home a newborn is one of life’s most profound moments—equal parts joy, wonder, and if we’re honest, a little overwhelm. The nursery needs setting up, the hospital bag needs packing, and there’s a seemingly endless list of tiny essentials you never knew existed.

This guide breaks down everything you truly need before, during, and after baby arrives. We’ve organized items by category, flagged the absolute must-haves, and noted what can wait. Whether you’re nesting at 30 weeks or scrambling in the final days, this checklist will help you feel prepared, confident, and ready to welcome your little one home.

What This Guide Covers:

Essential gear by category (feeding, sleeping, diapering, clothing, bathing, safety)

Hospital bag checklist for labor and delivery

Important documents and administrative tasks

Week-by-week preparation timeline

Budget-friendly alternatives and what not to buy

Evidence-based safety recommendations

Before Baby Arrives: The Essentials Checklist

Nursery and Sleep (Safe Sleep Foundation)

Must-Haves:

Crib or bassinet that meets current CPSC safety standards (slats no more than 2⅜ inches apart)

Firm, flat mattress with fitted sheets (3-4 sheets for frequent changes)

Waterproof mattress protector (2-3 for rotation during washing)

Sleep sacks or wearable blankets (avoid loose blankets per AAP safe sleep guidelines)

White noise machine (optional but helps many newborns settle)

Blackout curtains or shades for daytime naps

Baby monitor (audio minimum; video optional for peace of mind)

Safety Note: The American Academy of Pediatrics recommends room-sharing (but not bed-sharing) for at least the first 6 months, ideally the first year, to reduce SIDS risk by up to 50%.

Can Wait:

Decorative bedding sets (bumpers, pillows, blankets are unsafe for infants)

Changing table (you can use a changing pad on a dresser)

Glider or rocking chair (comfortable but not essential)

Water bottle (nursing makes you incredibly thirsty)

For Formula Feeding Families:

Must-Haves:

Baby bottles (4-6 bottles; 4-5 oz for newborns)

Bottle nipples (slow-flow for newborns; have backups)

Bottle brush and drying rack

Formula (start with small containers until you know what baby tolerates)

Bottle warmer (optional; warm water bath works too)

Insulated bottle carrier for outings

Note: If using powdered formula, CDC recommends preparing bottles fresh for each feeding for babies under 3 months, immunocompromised, or premature, to reduce infection risk.

High-sided bowls (for when you’re eating one-handed)

Snacks and easy meals stocked for postpartum recovery

Diapering Station

Must-Haves:

Diapers (newborn and size 1; babies go through 8-12 per day initially)

Baby wipes (unscented, sensitive skin formulas; or use warm water and soft cloths)

Diaper cream (zinc oxide-based for prevention and treatment of rash)

Changing pad (portable pads are great for multiple rooms)

Diaper pail or odor-sealing bags

Changing pad covers (2-3 washable covers)

Cloth Diapering Option:

24-36 cloth diapers (newborn or one-size adjustable)

4-6 diaper covers

Wet bag for storage

Cloth-safe detergent

Budget Tip: Store brands and generic diapers often perform just as well as name brands at 30-40% less cost. Buy small packs initially to test fit and absorption.

Onesies or bodysuits (6-8 in newborn and 0-3 month sizes; side-snap or kimono style easiest for newborns)

Sleepers with feet (4-6; zippers are faster than snaps at 3 AM)

Sleep gowns (2-3; great for nighttime diaper changes)

Hats (2-3 soft cotton hats; newborns lose heat through their heads)

Socks or booties (4-6 pairs; they fall off constantly)

Swaddle blankets (3-4 muslin or cotton swaddles, or 2-3 Velcro swaddles)

Going-home outfit (one special outfit plus a backup)

Seasonal outerwear (bunting or snowsuit for winter babies; sun hat for summer)

Sizing Reality Check: Many babies outgrow newborn size within 2-3 weeks. Stock more 0-3 month clothes than newborn.

Laundry Essentials:

Gentle, fragrance-free detergent (regular detergent is fine; “baby” formulas are optional)

Stain remover (enzyme-based for breast milk and formula stains)

Mesh laundry bags for small items like socks

Bathing and Grooming

Must-Haves:

Baby bathtub or sink insert (until baby can sit unassisted)

Soft washcloths (4-6 dedicated for baby)

Hooded baby towels (2-3; keep baby warm after bath)

Gentle baby wash and shampoo (tear-free, fragrance-free; can also use plain water for first month)

Baby lotion (fragrance-free; only if skin is dry—most newborns don’t need it)

Soft-bristle baby brush (for cradle cap)

Infant nail clippers or file (tiny nails grow fast and are sharp)

Digital thermometer (rectal is most accurate for newborns; have petroleum jelly on hand)

Bathing Frequency: Newborns only need 2-3 baths per week. Daily baths can dry delicate skin. Focus on keeping diaper area and skin folds clean between baths.

What NOT to Give: Never give honey to babies under 12 months (botulism risk), aspirin (Reye’s syndrome risk), or cough/cold medicines (not safe or effective for infants).

Extra underwear (hospital usually provides disposables, but bring backups)

Personal toiletries (toothbrush, shampoo, face wash, etc.)

Glasses or contacts (if you wear them)

Maternity pads (hospital provides some, but bring your preferred brand)

For Partner/Support Person:

Snacks and drinks (hospital cafeteria hours vary)

Change of clothes

Phone charger

Camera (if not using phone)

List of people to notify

For Baby:

Going-home outfit (in two sizes: newborn and 0-3 months)

Blanket for car ride

Properly installed car seat (hospital will check before discharge)

Hat and socks

What the Hospital Provides: Most hospitals supply diapers, wipes, basic toiletries, receiving blankets, hats, and initial formula if needed. Ask your provider what’s included.

Important Documents and Administrative Tasks

Before Baby Arrives

Insurance and Financial:

☐ Add baby to health insurance (usually must be done within 30 days of birth)

☐ Review maternity/paternity leave policies and complete paperwork

☐ Understand your insurance’s coverage for pediatric care and where to go for baby’s first appointments

☐ Review life insurance policies

☐ Update or create a will and designate guardianship

Healthcare Setup:

☐ Choose a pediatrician and schedule newborn appointment (usually within first week)

☐ Tour hospital or birth center

☐ Take childbirth class and infant care class

☐ Pre-register at hospital (usually done around 36 weeks)

How many diapers will my newborn use? Newborns typically use 8-12 diapers per day for the first few weeks, then 6-8 per day as they get older. Stock up on size 1 and 2; babies often skip newborn size entirely or outgrow it within two weeks.

What temperature should I keep the nursery? The AAP recommends 68-72°F (20-22°C) to reduce SIDS risk. Dress baby in layers you’d be comfortable in, plus one extra layer, and use a sleep sack instead of blankets.

How often should I bathe my newborn? 2-3 times per week is sufficient. Daily baths can dry out delicate newborn skin. Focus on keeping the diaper area, face, and neck folds clean with a warm washcloth between baths.

When should I start tummy time? Begin tummy time from day one for brief periods (2-3 minutes, 2-3 times daily) while baby is awake and supervised. This builds neck and shoulder strength and prevents flat spots on the head.

Can I use a baby wrap or carrier right away? Yes, as long as baby’s airway is clear and their face is visible. Ensure baby is in an ergonomic position with knees higher than bottom (M-position) and chin off chest.

What if my baby won’t sleep in the bassinet? This is common. Try swaddling, white noise, ensuring the room is dark and cool, and placing a worn shirt near baby (not over face) so they smell you. Always place baby on their back to sleep.

Do I really need to wake a sleeping baby to feed? In the first 2-3 weeks, yes, if baby hasn’t eaten in 3-4 hours during the day (2-3 hours at night for breastfed babies). After baby regains birth weight and pediatrician gives the okay, you can let baby sleep longer stretches.

What’s the best way to soothe a crying baby? Try the “5 S’s”: Swaddle, Side/stomach position (only while awake and supervised), Shush (white noise), Swing (gentle motion), and Suck (pacifier or nursing). Always check for basic needs first: hunger, diaper, temperature.

When can my baby meet visitors? This is a personal choice. Many families wait until after baby’s first vaccines (at 2 months) or limit visitors who aren’t up-to-date on Tdap and flu vaccines. Trust your instincts and don’t hesitate to set boundaries.

Preparing for a newborn is less about perfection and more about creating a safe, loving environment where your baby can thrive—and where you can rest and recover. You don’t need every gadget or the trendiest nursery theme. You need the basics, a support system, and permission to ask for help.

Remember:

Babies need surprisingly little—safe sleep space, food, clean diapers, and your love

Your instincts are powerful; trust yourself

Accept help when offered (meals, errands, holding baby while you shower)

Be kind to yourself in the postpartum period; recovery takes time

Every baby is different; what works for one may not work for yours

You’re already doing the most important work by preparing thoughtfully. Take a deep breath. You’ve got this.

This guide is for informational purposes only and does not substitute for medical advice from your pediatrician or healthcare provider. Always consult with qualified professionals for personalized guidance.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.

A new name marks a new chapter—but the paperwork can feel endless. This comprehensive guide gives you a clear, steady path through every step of the name change process. Whether you’re taking your spouse’s surname, hyphenating, or creating a new family name together, the administrative journey is similar. Follow the checklist, keep copies organized, and move at a calm, sustainable pace. You’ve got this.

According to recent data from the Pew Research Center, approximately 79% of women in heterosexual marriages still choose to take their spouse’s last name, while 14% hyphenate, and 5% keep their maiden name.[1] Regardless of your choice, updating your legal identity requires navigating multiple federal, state, and private institutions—each with their own requirements and timelines.

Before You Begin: Gather These Essentials

Critical Documents:

Certified copies of your marriage certificate (order 3–5 copies)

Request these from the county clerk where you were married

Cost typically ranges from $10–$30 per copy

Processing time: 2–4 weeks in most jurisdictions

Your current government-issued ID (driver’s license, state ID, or passport)

Social Security card (if in the U.S.)

Proof of residence (utility bill, lease agreement, or bank statement dated within the last 60 days)

A simple tracking sheet or folder for confirmations and dates

Optional but Helpful:

Passport-style photos (2–4 copies for various applications)

Digital copies of all documents stored securely in cloud storage

A dedicated email folder for name change confirmations

Notarized copies of your marriage certificate for international use

Understanding the Legal Framework

In the United States, name changes through marriage are governed by state law, but federal agencies like the Social Security Administration (SSA) and the Department of State set their own requirements for updating federal records.[2] Most states recognize a marriage certificate as sufficient legal documentation for a name change, eliminating the need for a court order—a significant simplification compared to name changes for other reasons.

Quick Note on Order and Timing

Critical Sequencing: In the U.S., update Social Security first, then your driver’s license/state ID, then your passport. This order matters because:

Social Security Administration (SSA) is the master federal database

DMV/State agencies verify your name against SSA records

Passport services cross-reference both SSA and state ID

Financial institutions validate against government IDs

Most other updates can follow in any order. Expect some agencies to require in-person appointments. Build a simple weekly plan so you’re not rushing—spreading updates over 4–8 weeks is perfectly normal and sustainable.

Processing Time Reference:

Social Security: Instant update in database, new card arrives in 7–10 days

Driver’s License: Same-day issuance in most states

Insurance providers: 1–3 business days for policy updates

Step-by-Step Name Change Checklist (U.S.)

1. Social Security Administration

What to do: File a name change with the Social Security Administration.

Why first: The SSA database is the authoritative source for your legal name. Other federal agencies, employers, financial institutions, and credit bureaus validate identity against SSA records. Updating this first prevents delays and rejections downstream.[4]

What you’ll need:

Form SS-5 (Application for a Social Security Card) – download from ssa.gov or pick up at any SSA office

Original or certified copy of your marriage certificate

Current government-issued photo ID (driver’s license, state ID, or U.S. passport)

How to complete:

In person: Visit your local SSA office (no appointment needed, but expect wait times)

By mail: Mail documents to your local office (only send certified copies, never originals except your current Social Security card)

Processing time: Your name is updated immediately in the system. Your new Social Security card arrives by mail in 7–10 business days.

Important tip: Request a printed receipt or confirmation with the date of your visit. Note this date in your tracking sheet—some DMVs ask when your SSA update was processed.

Special considerations:

If you’re updating both your name and gender marker, you’ll need additional documentation

Non-citizens may have additional requirements based on immigration status

If you’ve lost your Social Security card, you can replace it during the same visit

2. Driver’s License or State ID

What to do: Update your name at the Department of Motor Vehicles (DMV) or equivalent state agency.

Timing: Wait 24–48 hours after your SSA visit to ensure the database sync is complete, though many people successfully update the same day.

What you’ll need:

Updated Social Security confirmation (if available)

Current driver’s license or state ID

Certified marriage certificate

Proof of address (utility bill, bank statement, or lease dated within 60–90 days)

Texas: Accepts marriage certificate; new license issued immediately; $11 fee for duplicate license

New York: Can update online within 30 days of address change; otherwise in-person required

Florida: Requires in-person visit; no online option for name changes; first replacement free within 30 days of marriage[5]

Processing: Most states issue your new license immediately. Some provide a temporary paper license while your permanent card is mailed (7–14 days).

Helpful tip: Ask if you can update voter registration at the same visit—many states offer this convenience. Also inquire about organ donor registry updates if applicable.

3. U.S. Passport

What to do: Submit the appropriate passport application depending on when your current passport was issued.

Form selection:

Form DS-5504 (free): If your current passport is less than one year old

Form DS-82 ($130 fee): If your current passport is more than one year old but still valid

Form DS-11 ($130 fee + execution fee): If your passport is expired

What you’ll need:

Completed application form

Your current passport (will be canceled and returned to you)

Certified copy of your marriage certificate

One new passport photo (2×2 inches, taken within the last 6 months)

Payment for applicable fees

Submission methods:

By mail: Send to the National Passport Processing Center (for DS-5504 and DS-82)

In person: Required for DS-11 at a passport acceptance facility or agency

Processing times (as of 2026):[3]

Routine service: 8–11 weeks

Expedited service: 5–7 weeks (additional $60 fee)

Agency appointment: 5 business days (for urgent travel; requires proof of travel within 14 days)

Travel planning tip: If you have international trips planned within 6 months, start your passport update early. Always ensure the name on your flight booking matches the name on the ID you’ll carry. Some travelers maintain their maiden name passport until expiration to avoid booking complications.

4. Employer, Payroll, and Benefits

What to update:

HR/payroll system and employee records

Direct deposit information (often requires re-verification)

Health insurance enrollment

Retirement accounts (401k, 403b, pension)

Life insurance beneficiaries

Flexible Spending Accounts (FSA) or Health Savings Accounts (HSA)

Workplace email address and internal directory

Employee ID badge and building access cards

Professional email signature

Process: Contact your HR department as soon as your SSA update is complete. Most companies require:

A copy of your marriage certificate

Your new Social Security card (once received)

Updated Form W-4 if changing withholding status

Beneficiary designation forms if updating

Timeline: HR updates typically process within 1–2 pay periods. Verify your next paycheck stub shows your new legal name.

Important considerations:

Update your name before open enrollment to avoid insurance coverage gaps

Confirm your W-2 (issued in January) will reflect your legal name for tax filing

If you have stock options or equity grants, verify these are updated to prevent future complications

Request written confirmation from HR and save it to your documentation folder

5. Banks, Credit Cards, and Financial Institutions

What to update:

Checking and savings accounts

Credit cards (personal and business)

Mortgage or home equity loans

Auto loans and leases

Student loans

Personal loans

Investment accounts (brokerage, IRA, Roth IRA)

Cryptocurrency exchange accounts

Payment apps (Venmo, PayPal, Cash App, Zelle)

What you’ll need:

Valid government-issued ID with new name

Certified copy of marriage certificate

Account numbers for each institution

Bank-specific forms (often available online or in-branch)

Process:

In person: Visit your primary bank branch with documents; they can often update all accounts simultaneously

By phone: Call customer service; may require mailing or uploading documents

Online: Some institutions allow secure document upload through their portals

Timeline: Most banks process name changes within 3–5 business days. New debit/credit cards typically arrive within 7–10 days.

Critical follow-up steps:

Order new checks with your new name

Verify all automatic payments, direct deposits, and recurring transfers continue uninterrupted

Update your name in mobile banking apps

Confirm your credit report reflects the name change (more on this below)

Credit reporting agencies: Your creditors will report your name change to the three major credit bureaus (Equifax, Experian, TransUnion), but you can also notify them directly:

The agencies will link your new and old names to your credit history

Your credit score and history remain intact

Request a free credit report 30 days after updates to verify accuracy[6]

6. Insurance Providers

Types of insurance to update:

Health insurance (individual and employer-sponsored)

Dental and vision insurance

Auto insurance

Homeowners or renters insurance

Life insurance

Disability insurance (short-term and long-term)

Umbrella liability insurance

Professional liability insurance (if applicable)

What you’ll need:

Policy numbers

Copy of marriage certificate

New driver’s license (for auto insurance)

Insurer-specific forms

Why it matters: An incorrect name on your insurance card can cause claims to be denied or delayed. Medical providers verify your identity against your insurance card, and any mismatch can create billing complications.[7]

Process:

Contact each insurance provider’s customer service

Many allow online updates through member portals

Request updated insurance cards and policy documents

Ask if the name change triggers any policy document reissuance

Timeline: Most insurance updates process within 1–3 business days. New insurance cards arrive within 7–10 days.

Important tip: Keep PDFs of all updated policy documents together in a dedicated digital folder. Update your insurance information in your phone’s emergency contact settings.

7. IRS and Tax Filing

What you need to know: The Internal Revenue Service (IRS) pulls your legal name from Social Security Administration records. Once your SSA name is updated, your tax filings should match automatically.[8]

Action items:

Verify your W-2 reflects your new legal name before year-end

If filing jointly, ensure both spouses’ names match SSA records

Update your name with your tax preparer or tax software account

If you file business taxes (1099, Schedule C), update your business entity records

Special consideration for newlyweds: If you married late in the tax year and haven’t completed your SSA name change before filing, you have two options:

File under your maiden name (matching your SSA record at year-end)

Complete your SSA update first, then file with your new name

Filing with a name that doesn’t match SSA records can delay refund processing by 6–8 weeks.

State taxes: Don’t forget to update your name with your state tax agency as well, especially if you file state returns separately.

8. Voter Registration

What to do: Update your voter registration to reflect your new legal name and current address.

Why it matters: Voter registration databases must match your current legal name and address for you to receive ballots and vote without complications.[9]

How to update:

At the DMV: Many states allow simultaneous voter registration updates during your driver’s license visit

Online: Most states offer online voter registration updates through their Secretary of State website

By mail: Download and mail a voter registration form

In person: Visit your county elections office

State-specific resources:

National: vote.gov provides links to each state’s registration portal

Deadlines: Check your state’s voter registration deadlines before elections

Timeline: Updates typically process within 2–4 weeks. You should receive a new voter registration card confirming your updated information.

9. Professional Licenses and Certifications

What might need updating:

State professional licenses (medical, legal, nursing, teaching, real estate, cosmetology, etc.)

Industry certifications (CPA, PE, PMP, etc.)

Professional association memberships

Bar association registration (for attorneys)

Medical board registration (for physicians)

Continuing Education (CE) transcripts and records

Process: Each licensing board has unique requirements. Most require:

Official name change request form

Copy of marriage certificate

Current license number

Reissuance fee (typically $20–$75)

Important considerations:

Lead times: Some boards take 4–8 weeks to process name changes

Certificate reissuance: Ask if a formal reissued certificate is required or if a database update suffices

Wall certificates: Some professions require new wall certificates for display in offices

CE credits: Verify your continuing education credits transfer to your new name without issue

Tip: Start professional license updates early in your name change process, as these often have the longest processing times.

10. Utilities and Household Accounts

What to update:

Electric and gas utilities

Water and sewer services

Trash and recycling collection

Internet service provider

Cable or satellite TV

Mobile phone account

Landline (if applicable)

Home security system

Streaming services (Netflix, Hulu, Spotify, etc.)

Smart home device accounts (Alexa, Google Home, Ring, Nest)

Process:

Most utilities allow name changes via phone or online account portal

Some may require a copy of your marriage certificate

Joint accounts: Decide if you want individual or joint account holder status

Why it matters: Utility accounts in your legal name help establish proof of residence for other updates. They also ensure billing accuracy and credit reporting (if applicable).

Helpful tip: Take screenshots of your account settings before making changes. This allows you to verify all services, auto-payments, and account preferences transferred correctly.

11. Medical Providers, Schools, and Pharmacies

Healthcare providers to notify:

Primary care physician

Specialists (cardiologist, dermatologist, etc.)

Dentist and orthodontist

Eye doctor

Mental health therapist or psychiatrist

Physical therapist

Chiropractor

Patient portals (MyChart, FollowMyHealth, etc.)

Pharmacy updates:

Retail pharmacy (CVS, Walgreens, etc.)

Mail-order prescription services

Pharmacy benefit manager (PBM)

What you’ll need:

New government ID

Updated insurance card

Marriage certificate (some offices may request)

Process:

Call each provider’s office to update records

Bring your new ID and insurance card to your next appointment

Update your name in patient portals yourself or request staff assistance

Why it matters: Accurate patient records prevent prescription errors, insurance claim denials, and medical record mix-ups. Your pharmacy profile must match your insurance exactly for coverage to process correctly.[10]

Educational institutions: If you’re currently enrolled in school or continuing education, update:

Student records and ID

Financial aid accounts (FAFSA)

Student loan servicers

University email and portal access

Library card

Alumni association records

12. Travel Programs and Loyalty Accounts

TSA PreCheck and Global Entry:

TSA PreCheck: Update through the Universal Enrollment Services website or by visiting an enrollment center

Global Entry, NEXUS, SENTRI: Update through your Trusted Traveler Programs (TTP) account

No fee for name changes, but you must update before your next trip

Failure to update can result in denial at security checkpoints

Airline loyalty programs:

Frequent flyer accounts (American AAdvantage, Delta SkyMiles, United MileagePlus, etc.)

Update through airline websites or customer service

Critical: The name on your booking must match your ID exactly—even middle initials matter

Hotel and car rental programs:

Hotel loyalty (Marriott Bonvoy, Hilton Honors, IHG Rewards, etc.)

Car rental (Hertz Gold, Enterprise Plus, National Emerald Club, etc.)

Vacation rental profiles (Airbnb, VRBO)

Other travel accounts:

Travel credit cards (update through your card issuer)

Critical tip: Complete all travel program updates before booking new trips. Name mismatches can prevent boarding and are expensive to correct last-minute.

13. Vehicle Titles, Registration, and Property Deeds

Vehicle updates:

Vehicle title: Update through your state DMV

Vehicle registration: Often updated simultaneously with title

Auto loan: Notify your lender (bank or credit union)

Car insurance: (covered in Insurance section above)

Process varies by state:

Some states require in-person visits

Others allow mail-in forms

Fees typically range from $15–$50

May require current title, marriage certificate, and ID

Property and real estate:

Home deed: Generally does not require updating immediately—your legal name is what matters, and a marriage certificate proves the connection

Mortgage: Notify your mortgage servicer (especially for payment matching)

Property tax records: Update with your county assessor

Homeowners insurance: Update with your insurance provider

HOA records: Notify your homeowners association

Trusts and estate planning documents: If you have:

Living trusts

Wills

Power of attorney documents

Healthcare directives

Beneficiary designations

Consult with an estate planning attorney to determine if amendments or restatements are necessary. In most cases, a marriage certificate connects your previous and new identity, but complex trusts may require formal updates.

14. Digital Life and Online Accounts

Email accounts:

Update display name in Gmail, Outlook, Yahoo, etc.

Consider creating a new email with your married name

Set up forwarding if transitioning email addresses

Update email signatures

Social media profiles:

Facebook, Instagram, Twitter/X, LinkedIn, TikTok

Update profile names, usernames (if desired), and about sections

Privacy consideration: You can keep your maiden name on social media if preferred

Cloud storage and productivity:

Google Drive, iCloud, Dropbox, OneDrive

Microsoft 365, Google Workspace accounts

Password managers (LastPass, 1Password, Dashlane)

E-commerce and shopping:

Amazon, eBay, Etsy

Online grocery delivery (Instacart, Shipt)

Retail accounts (Target, Walmart, etc.)

Subscription boxes and auto-deliveries

E-signature and legal:

DocuSign, HelloSign, Adobe Sign

Online notary services

Legal document platforms

Subscriptions and memberships:

Streaming services (covered above)

Gym and fitness memberships

Professional networking sites

Magazine and newspaper subscriptions

Warehouse clubs (Costco, Sam’s Club)

Tip: Prioritize accounts where your legal name is required for payments or legal documents first, then update social and display names at your leisure.

Printable Mini-Checklist

Phase 1: Core Identity (Week 1-2)

☐ Social Security Administration

☐ Driver’s license/State ID

☐ Passport (if traveling internationally within 6 months)

☐ Voter registration

Phase 2: Work and Money (Week 2-3)

☐ Employer/payroll/benefits

☐ Banks and credit unions

☐ Credit cards

☐ Loans and mortgages

☐ Investment and retirement accounts

Phase 3: Insurance and Taxes (Week 3-4)

☐ Health insurance

☐ Dental and vision insurance

☐ Auto insurance

☐ Homeowners/renters insurance

☐ Life insurance

☐ Disability insurance

☐ IRS (via SSA automatic update)

Phase 4: Professional and Property (Week 4-6)

☐ Professional licenses

☐ Vehicle title and registration

☐ Property deeds (if needed)

☐ Trusts and estate documents

Phase 5: Daily Life (Week 5-8)

☐ Utilities (electric, gas, water)

☐ Phone and internet

☐ Streaming services

☐ Medical providers

☐ Dentist

☐ Pharmacy

☐ Veterinarian (for pet records)

Phase 6: Travel and Leisure (Week 6-8)

☐ TSA PreCheck/Global Entry

☐ Airline loyalty programs

☐ Hotel rewards programs

☐ Car rental memberships

Phase 7: Digital Life (Ongoing)

☐ Email display names

☐ Social media profiles

☐ Cloud storage accounts

☐ E-signature services

☐ E-commerce accounts

☐ Subscription services

How Long Will This Take?

Fast track: 2–3 weeks If you batch appointments, prep all documents in advance, and dedicate several full days to the process. This approach works well if you have time off after your wedding or honeymoon.

Standard pace: 4–8 weeks A steady, sustainable approach with minimal disruption to work and life. This is the recommended timeline for most people.

Extended timeline: 8–12 weeks If you’re traveling frequently, have complex professional licenses, or prefer spreading tasks across several months.

Time management tip: Schedule 90-minute focused blocks once or twice a week. Each block: one major agency visit or phone call + two quick online account updates. This rhythm prevents burnout and maintains progress.

Common Pitfalls (and How to Avoid Them)

1. Not ordering enough certified copies

The problem: Many agencies require original or certified copies of your marriage certificate. Ordering one or two copies forces you to wait for documents to return before proceeding to the next step.

The solution: Order 3–5 certified copies upfront. At $10–$30 per copy, this small investment saves weeks of waiting. Most counties allow online ordering through their vital records office.

2. Updating travel documents last-minute

The problem: Passport processing takes 8–11 weeks (5–7 weeks expedited). If you book international travel before updating your passport, you’ll face a name mismatch.

The solution: Align your ID updates with your travel calendar. If you have trips planned, either:

Complete your passport update well in advance (3+ months before travel)

Book travel under your maiden name until your new passport arrives

Maintain consistency: name on ticket = name on traveling ID

3. Losing track of confirmations

The problem: When updating 20+ institutions, it’s easy to forget what’s done, what’s pending, and when you made each update. This causes duplicate efforts and missed updates.

The solution: Create a single tracking system (digital or physical):

Spreadsheet with columns: Institution, Date Contacted, Confirmation Number, Date Completed, Notes

Dedicated email folder for all confirmation emails

Cloud folder (Google Drive, Dropbox) for all documentation

4. Skipping professional licenses

The problem: Professional licensing boards often have 4–8 week processing times and specific requirements. Forgetting these can cause legal complications if you sign documents professionally.

The solution: Identify all licenses and certifications early. Start these updates in week 1 alongside Social Security. Create calendar reminders for any required continuing education or renewal dates.

5. Forgetting about automatic payments

The problem: When your bank issues a new credit or debit card with your new name, your old card number may be deactivated, breaking automatic payments.

The solution: Before requesting new cards, screenshot or document all automatic payments. After receiving new cards, systematically update each merchant. Check your bank statements for 2–3 months after to catch any failed payments.

6. Neglecting credit reports

The problem: Credit bureaus sometimes create separate profiles for different name variations, potentially fragmenting your credit history.

The solution: 30 days after completing bank and credit card updates, pull your free annual credit report from all three bureaus (annualcreditreport.com). Verify:

Your new and old names are properly linked

All accounts appear under your profile

No errors or fraudulent accounts exist

7. Rushing the Social Security update

The problem: The SSA database is the foundation. Rushing to the DMV before the SSA update fully processes can cause rejections or delays.

The solution: Wait 24–48 hours after your SSA visit before attempting DMV updates. This gives the system time to synchronize. If visiting the DMV immediately, bring your SSA receipt as proof of update.

State-Specific Considerations

Name change requirements vary by state. Here are some notable differences:

Community Property States: In Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin, special rules may apply to property ownership and name changes on deeds.[11]

States with Online DMV Name Changes: A growing number of states allow online driver’s license updates for name changes:

Arizona (with requirements)

Georgia (within 30 days of address change)

Illinois (limited circumstances)

Check your state DMV website for current options

States Requiring In-Person DMV Visits: Most states still require in-person visits for name changes:

California, Texas, Florida, New York, Pennsylvania (among others)

Bring all required documents to avoid multiple trips

Passport Agencies by Region: For urgent passport needs (travel within 14 days), you can visit a regional passport agency:

Boston, Chicago, Detroit, Honolulu, Houston, Los Angeles, Miami, Minneapolis, New Orleans, New York City, Philadelphia, San Francisco, Seattle, Washington DC

Appointment required; proof of urgent travel necessary[3]

International Considerations

If you’re a dual citizen:

Update your name with both countries’ passport agencies

Requirements and timelines vary significantly by country

Some countries don’t recognize name changes after marriage

If you plan to travel internationally:

Ensure your airline ticket name matches your passport exactly

Some countries require a visa with your legal name

Carry a certified copy of your marriage certificate when traveling during transition periods

If you’re married abroad:

You may need to register your foreign marriage certificate with your home country

Some states require an apostille (international certification) on foreign marriage certificates

Contact your county clerk for specific requirements

Timeline for International Name Changes (Common Countries)

United Kingdom: 2–3 weeks for passport update

Canada: 20 business days for passport; varies by province for driver’s license

Australia: 2–3 weeks for passport; varies by state for license

European Union: Varies by country; typically 4–8 weeks

Special Situations

Hyphenating Your Last Name

If you’re hyphenating (e.g., Smith-Jones):

Use the exact same hyphenation format everywhere

Computer systems sometimes read hyphens differently

Be consistent: Smith-Jones vs. Smith Jones vs. SmithJones

Professional tip: Use the hyphenated form as your legal name, but you can use a shortened version professionally

Keeping Your Maiden Name Professionally

Many people maintain their maiden name for professional purposes:

Use your legal name for: government IDs, taxes, insurance, financial accounts

Use your professional name for: work email, publications, professional licenses, social media

Disclose your legal name to HR and licensing boards

This is completely legal and increasingly common

LGBTQ+ Couples and Name Changes

Same-sex couples have the same legal right to change names through marriage:

The process is identical regardless of gender

If both partners are changing names or creating a new combined surname, both will update through the same process

Some couples choose to both take a hyphenated combination

Changing Your Child’s Last Name

If you have children from a previous relationship:

Changing a child’s last name is a separate legal process

Usually requires consent from both legal parents

May require a court order

Consult with a family law attorney for your specific situation

Financial and Legal Protections

Protecting Your Identity During Transition

During the name change process, you may have:

Multiple valid IDs with different names

Credit accounts under two names

Professional records split across identities

To protect yourself:

Keep certified copies of your marriage certificate readily accessible

Maintain a file with old and new IDs during transition periods

Monitor your credit reports for suspicious activity

Use strong, unique passwords for all financial accounts

Enable two-factor authentication wherever possible

Consider a credit freeze during the transition if you’re concerned about identity theft

Tax Implications

Generally, there are no tax implications to changing your name, but keep these in mind:

Your tax filing name must match SSA records

If filing jointly, both spouses’ names must match SSA records

Mismatches can delay refund processing

Update your name before year-end to simplify tax season

Recommendation: Schedule a consultation with your estate planning attorney within 6 months of your marriage to review all documents.

Frequently Asked Questions

Do I need to change my name everywhere?

No. You’re required to update your name where your legal identity, finances, or benefits depend on it (government IDs, banks, insurance, employment). Display names on social media and informal accounts can wait or remain unchanged if you prefer.

What if I’m hyphenating or keeping my maiden name professionally?

This is increasingly common. Use your legal name for government agencies, financial institutions, and anywhere legal identity verification occurs. Use your preferred professional name for work-related platforms, publications, and brand-facing contexts. Be transparent with HR and licensing boards about both names.

Do I need a lawyer?

Usually no. Marriage-based name changes are straightforward and don’t require legal assistance. However, consider consulting a professional for:

Professional licensing in regulated fields (medical, legal)

International name changes or dual citizenship issues

Changing children’s names from previous relationships

Can I keep traveling during the process?

Yes—just ensure the name on your booking matches the ID you’ll carry for that trip. Options:

Book under your maiden name and travel with your old ID (if still valid)

Wait until you receive your new passport to book with your married name

Carry your marriage certificate as proof of name change if using mixed documents (not guaranteed to work—airline discretion)

What if my Social Security update doesn’t show immediately at the DMV?

Wait 24–48 hours for database synchronization. If you’re at the DMV and facing issues, showing your SSA receipt sometimes allows processors to manually verify. If rejected, simply return in 1–2 days.

How do I change my name on my birth certificate?

You don’t. Birth certificates are historical documents and are never updated for name changes. Your marriage certificate serves as legal proof connecting your birth name to your married name.

What if I get divorced and want to reclaim my maiden name?

Your divorce decree typically includes provisions for name restoration. The process is similar to a marriage name change: update SSA first, then DMV, then cascade through other institutions. You’ll use your divorce decree as the legal documentation instead of a marriage certificate.

Can I change to a completely new name through marriage?

State laws vary. Most states allow you to take your spouse’s surname, hyphenate, or combine names. Creating an entirely new surname (not derived from either partner) may require a formal court-ordered name change in some jurisdictions. Check your state’s specific laws.

What happens to my professional publications under my maiden name?

They remain under your maiden name. Many professionals:

Continue publishing under their maiden name

Use both names with “née” (e.g., Dr. Jane Smith née Johnson)

Include both names in author profiles

Create a professional CV that bridges both identities

Will changing my name affect my credit score?

No. Your credit history is tied to your Social Security number, not your name. Credit bureaus will link both names to your single credit profile. Your score and history remain intact.[6]

How do I handle the transition period when I have IDs with different names?

Keep your marriage certificate accessible at all times. If questioned, it’s legal proof connecting both identities. During the 2–8 week transition, you may encounter:

Insurance cards with your old name but prescriptions requiring new ID

Bank cards with your old name but checks with your new name

Mismatched IDs for travel

These are normal and expected. Most institutions understand and accommodate the transition period.

[2] Social Security Administration (2025). “Social Security Number and Card: How to Change Your Name.” https://www.ssa.gov/ssnumber/

[3] U.S. Department of State (2026). “Passport Processing Times and Name Changes.” Bureau of Consular Affairs.https://travel.state.gov/

[4] National Association of Social Security Claimants’ Representatives (2024). “Understanding Social Security Records and Identity Verification.” https://www.nosscr.org/

[5] American Association of Motor Vehicle Administrators (2025). “State Requirements for Driver License Name Changes.” https://www.aamva.org/

To make your name change process even smoother, consider using these tools:

Tracking Spreadsheet Template: Create a spreadsheet with these columns:

Institution/Agency Name

Category (Government, Financial, Insurance, etc.)

Priority (High, Medium, Low)

Date Contacted

Method (In-person, Phone, Online)

Confirmation Number

Date Completed

Notes

Follow-up Required (Yes/No)

Document Checklist:

☐ Marriage certificate ordered (quantity: ___)

☐ Marriage certificate received (date: ___)

☐ Current driver’s license (expires: ___)

☐ Current passport (expires: ___)

☐ Social Security card located

☐ Passport photos taken (date: ___)

☐ Proof of residence documents gathered

☐ Tracking folder created (digital/physical)

Closing: A Steady Finish

This isn’t a sprint—it’s a sequence. Your name change journey is personal, and there’s no single “right” timeline. Some people complete everything in two weeks; others spread it across three months. Both approaches are valid.

Remember:

Move one step at a time

Save every confirmation

Celebrate progress as you go

Ask for help when you need it (HR departments, DMV clerks, and customer service representatives handle name changes daily)

Be patient with yourself during the transition

Your new name deserves a calm, confident arrival in every corner of your life. Marriage is a beautiful milestone, and while the paperwork feels administrative, it’s part of weaving your identities together legally, financially, and socially.

Final encouragement: Thousands of people navigate this process every day. Government agencies and private institutions have well-established procedures. You’re not alone, and you’re fully capable of completing this journey successfully.

Take a deep breath, pull out your tracking sheet, and tackle your first item. Before you know it, you’ll be signing documents with your new name like you’ve had it your whole life.

Congratulations on your marriage, and best wishes as you step into this new chapter—paperwork and all.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.

Moving day can feel overwhelming when you’re juggling dozens of tasks at once. A solid moving day checklist keeps you organized and prevents the last-minute scramble that catches most people off guard.

Here at LifeEventGuide, we’ve seen how a structured approach transforms a stressful move into a manageable process. This guide walks you through every phase, from weeks before you pack your first box to settling into your new place.

Getting Started: The First Weeks Matter Most

Build Your Timeline and Budget

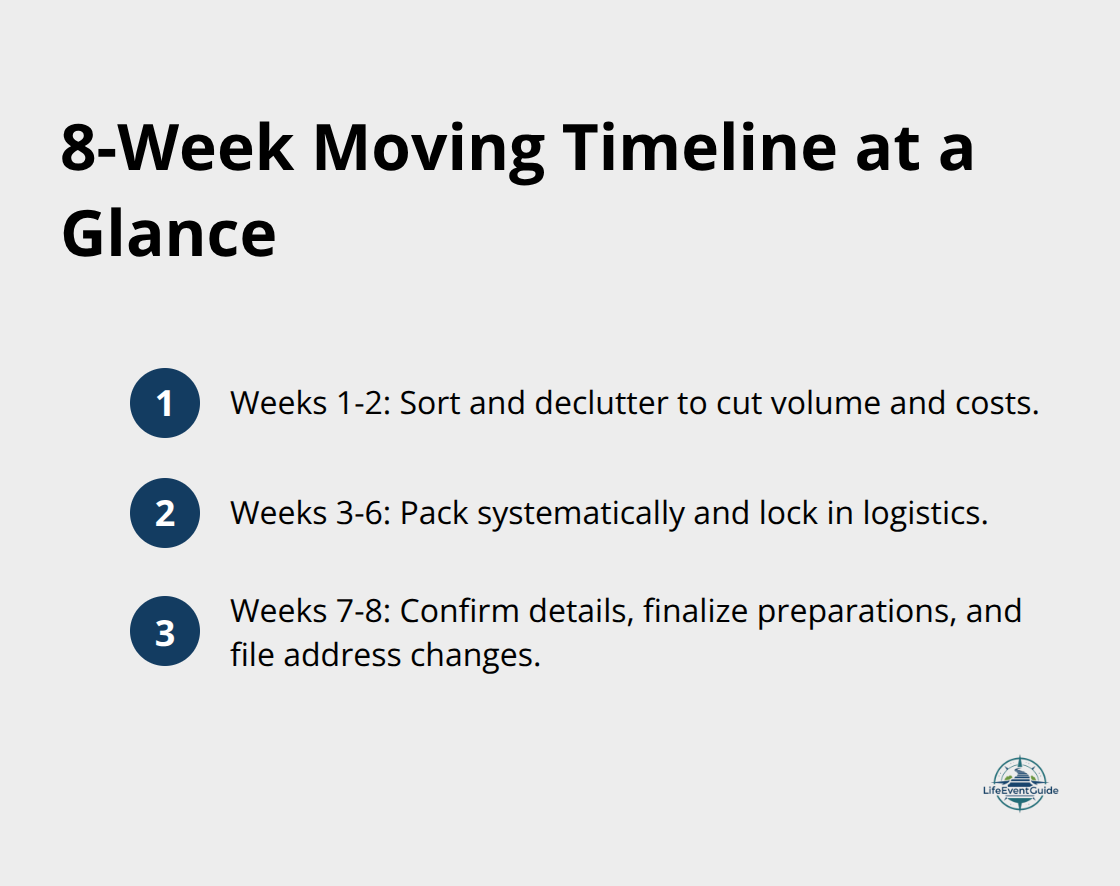

Starting your move weeks in advance separates organized transitions from chaotic ones. Work backward from your move date to create a realistic timeline. If you’re moving in eight weeks, allocate the first two weeks to sorting and decluttering, the next four to packing and logistics, and the final two to final preparations and address changes. This pacing prevents the cramped feeling of last-minute decisions.

Your timeline must include specific dates for contacting moving companies, changing your address with the USPS, and notifying utilities. Many people underestimate how long these administrative tasks take-transferring medical records, coordinating with your old and new utility providers, and updating your address across banks, insurance companies, and subscription services typically requires two to four weeks of scattered effort.

Build your budget around three main categories: moving services, supplies, and setup costs at your new home. Request on-site estimates from at least three moving companies and verify each company’s USDOT number with the U.S. Department of Transportation to confirm registration and safety standards. Professional movers typically cost between $1,400 and $9,700 for a full-service move, though prices vary based on distance and volume. If you’re renting a truck instead, factor in fuel, insurance, and equipment rental fees. Add 15 to 20 percent to your initial estimate as a buffer for unexpected costs.

Sort Your Belongings and Measure Your New Space

Decluttering before packing reduces moving expenses because costs increase with volume. Sort your belongings into three categories: keep, donate, and discard. Items you haven’t used in two years rarely deserve space in your new home.

Measure doorways and rooms in your new place to verify that large furniture will actually fit. This prevents the frustration of discovering a couch won’t navigate through a hallway or a bed won’t fit through a bedroom door. Once you’ve decided what travels with you, finalize your moving company choice and get written confirmation of the date, costs, and specific services included. The written estimate protects both you and the mover by establishing clear expectations.

Secure Your Moving Company and Declare Valuables

If you have items worth over $100 per pound, declare them to your mover and consider additional insurance coverage, as standard policies have per-item limits. Confirm all arrangements two weeks before moving day and provide your mover with complete old and new addresses plus multiple contact numbers. This level of detail prevents day-of confusion and missed appointments. With your timeline locked in and your mover confirmed, you can now focus on the physical work of preparing your home and items for transport.

Packing and Logistics: Getting the Details Right

Pack Room by Room with a Consistent System

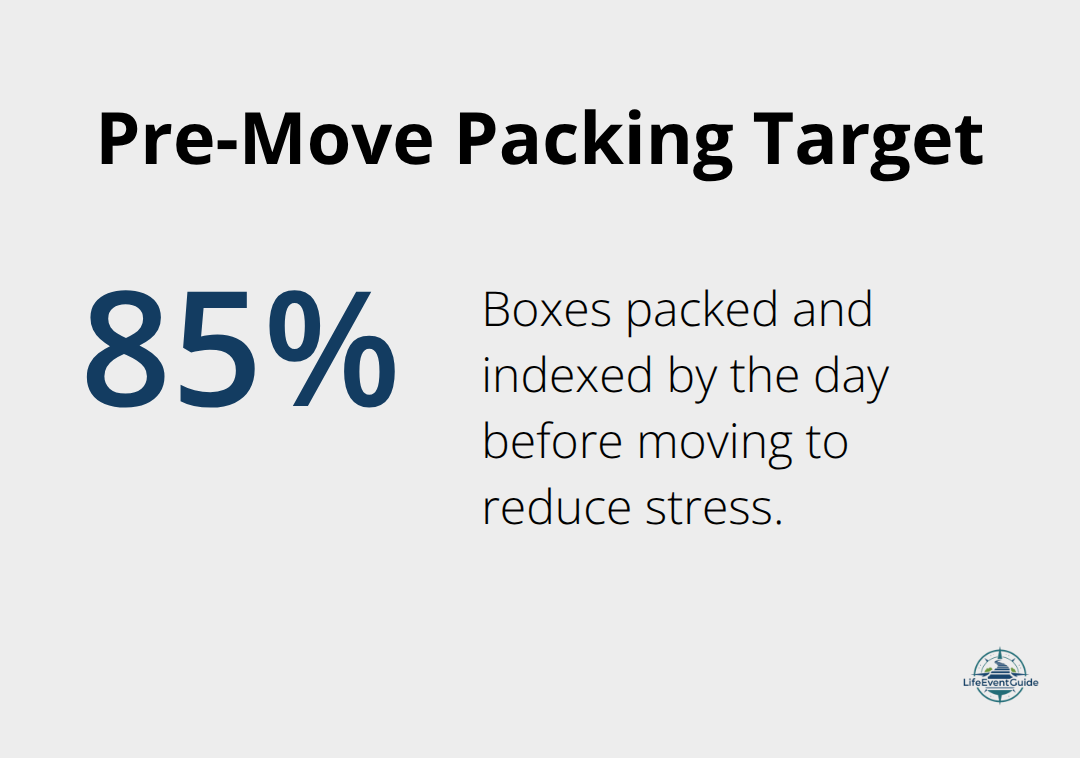

Packing room by room with a consistent system prevents items from scattering across boxes without clear destinations. Start with spaces you use least frequently-guest bedrooms, storage closets, seasonal decorations-so daily disruptions stay minimal. Try to have roughly 85 percent of your boxes packed and indexed by the day before moving rather than chasing perfection in those final chaotic hours. Create a single numbering system across all rooms and maintain one master box index that logs contents and destinations. This approach takes discipline but saves hours on moving day when locating a specific item could otherwise mean unpacking dozens of boxes.

Number each box with a permanent marker on both the top and side so contents remain visible regardless of stacking position. When packing room by room with a consistent system, place heavier boxes at the bottom to stabilize the load and avoid crushing lighter items, with lighter, more delicate items on top. Dish barrels and wardrobe boxes, which you can order when requesting moving company estimates six weeks before your move, protect fragile kitchen items and hanging clothes far better than improvised solutions.

Label Boxes and Create a Color-Coded System

Labeling extends beyond writing contents on boxes. Create a color-coded system using brightly colored labels or markers to assign each room a specific color, then apply that color to every box destined for that space. Movers move faster and more accurately when they can spot a red label means master bedroom without reading individual labels. This visual system reduces confusion and accelerates the unloading process significantly.

Update Utilities and Address Information

Update utilities and address changes during weeks three through six of your timeline to avoid service gaps. Contact your electricity, gas, water, phone, and internet providers simultaneously rather than staggering calls, since coordination schedules installation around your moving date. Set up new accounts before canceling old ones to prevent lapses, especially for internet service.

The USPS Change of Address form processes within three to five business days, so submit it four weeks before moving. Simultaneously notify banks, credit card companies, insurance providers, subscription services, and the IRS using a simple spreadsheet tracking which entities you’ve contacted and when. Medical records transfers typically require written release forms and take two to four weeks, so initiate these requests at the six-week mark. Forward mail from your old address to your new one for at least six months to catch payments and notices that arrive late.

With your boxes labeled, your utilities coordinated, and your address changes submitted, you’ve completed the groundwork that prevents moving day surprises. The final preparation phase focuses on the items and documents that require special handling during the actual move.

What to Protect on Moving Day

Secure Your Most Valuable Possessions

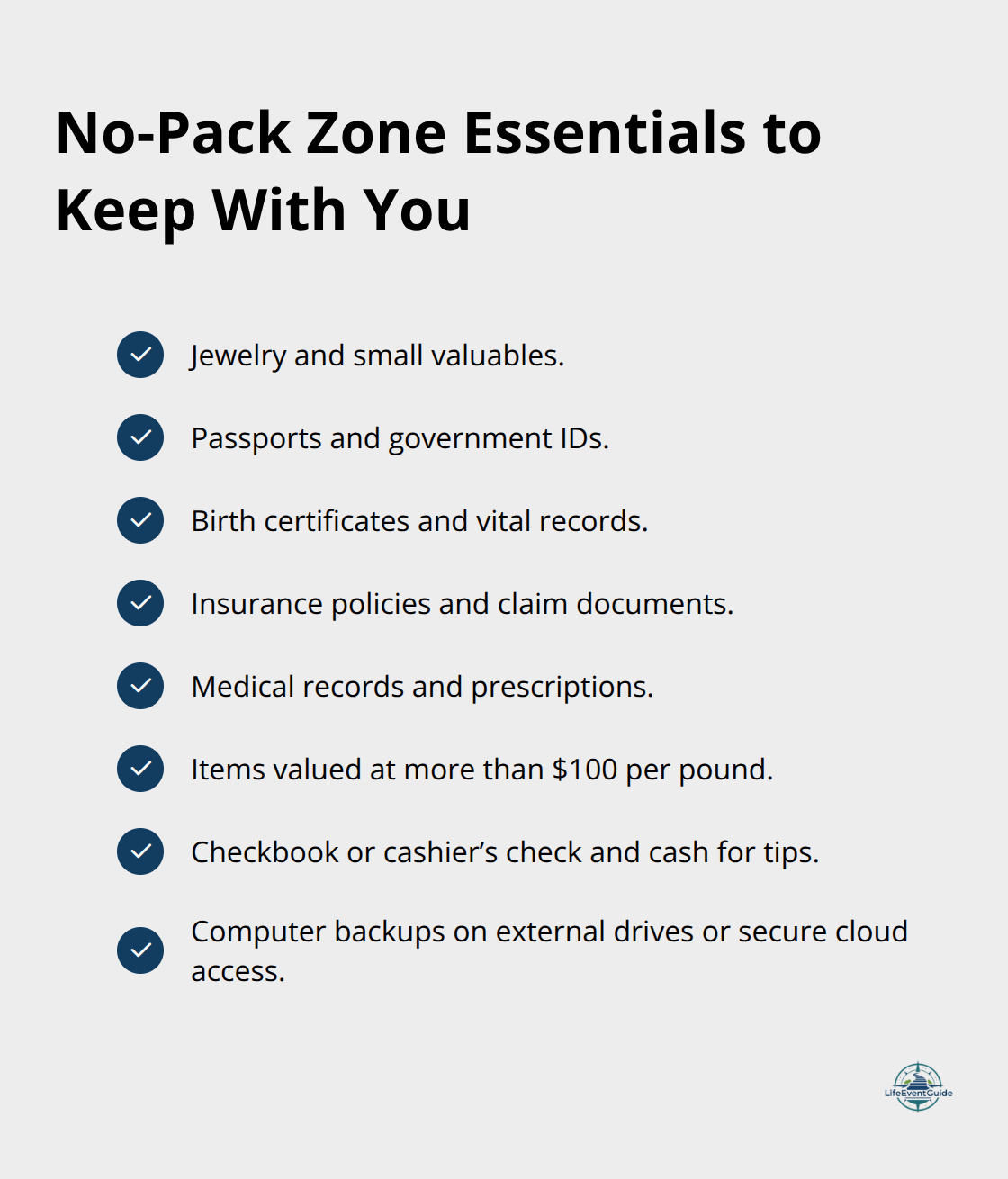

The 24 hours surrounding your move require a different mindset than the weeks of preparation that came before. While movers handle the bulk of your possessions, certain items demand your personal attention and control. Keep all important documents, valuables, and irreplaceable items with you rather than on the moving truck. This means your jewelry, passports, birth certificates, insurance policies, medical records, and any items worth more than $100 per pound travel in your vehicle or stay in your direct possession.

Create a secure case or lockbox for jewelry and store computer backups on external drives or cloud storage that you transport yourself. Your checkbook must remain accessible and unpacked-you’ll need it to pay the movers with a cashier’s check or money order on arrival, plus cash for tips ranging from 10% to 20%, up to $100 per mover.

Establish a No-Pack Zone