Buying a used car without checking its history is like walking into a deal blind. A vehicle history report checklist helps you spot hidden problems before you hand over your money.

At LifeEventGuide, we know that past accidents, title issues, and maintenance gaps can cost you thousands in repairs down the road. This guide walks you through what to look for and how to use these reports to make a smarter purchase.

Why Vehicle Reports Matter

Hidden Damage Costs More Than You Think

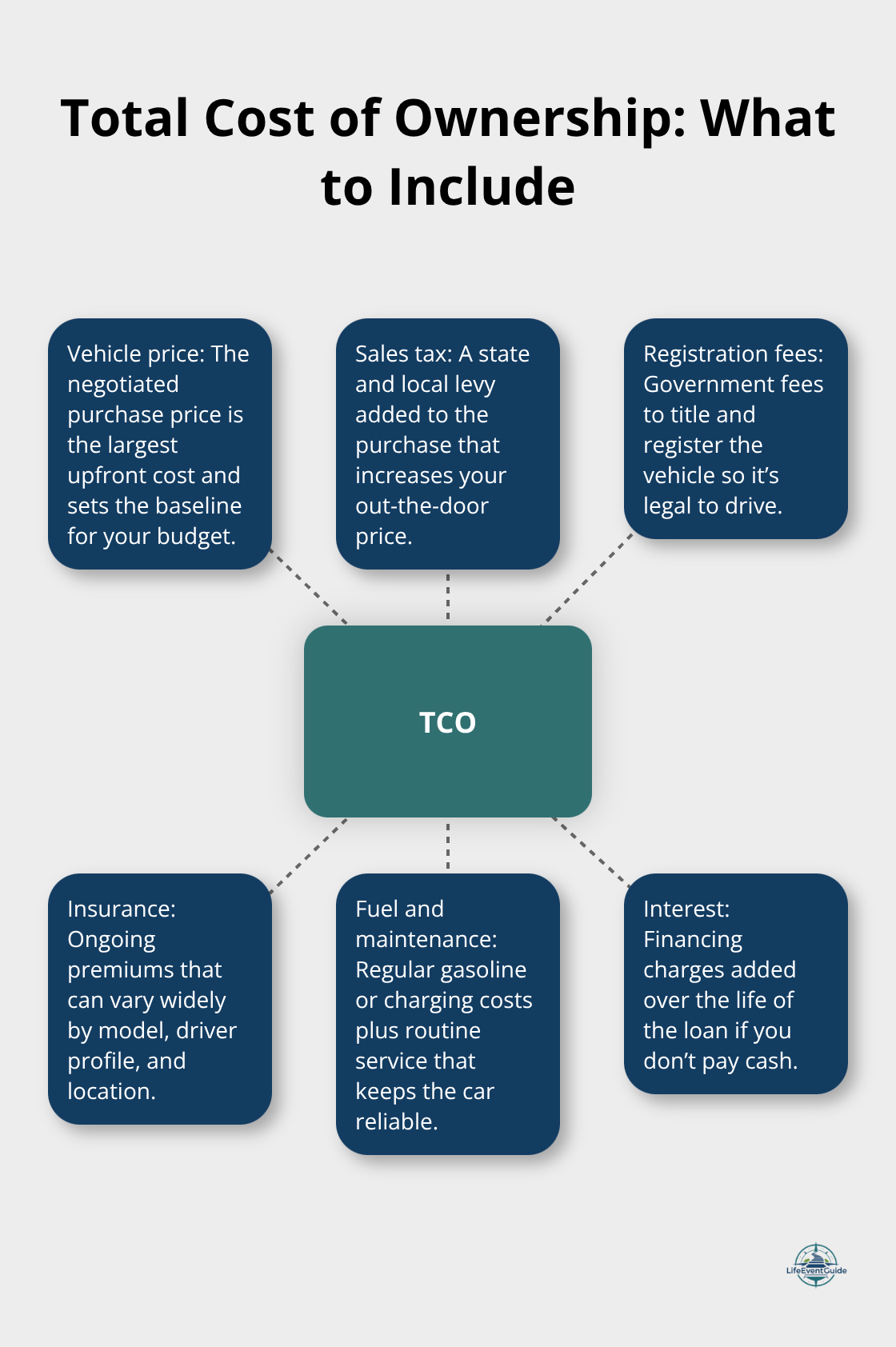

A vehicle history report is your first line of defense against buying someone else’s problem. When you pull a report from Carfax or AutoCheck, you access data from thousands of sources-insurance companies, police records, service shops, and auction houses-that collectively reveal what actually happened to that car. These reports cost between $25 and $45 for a single lookup, a small price compared to the thousands you might spend fixing hidden damage later.

Hidden accident damage represents the most expensive surprise you can encounter after purchase. A vehicle that experienced a major collision but underwent repair may pass a quick visual inspection and still drive fine for months before structural issues emerge. The damage hides beneath the surface, affecting frame integrity and safety systems that won’t fail until months or years later.

Service Records Show You the Real Story

Service records tell you whether the previous owner actually maintained the vehicle or ignored it. A car with a complete service history-showing regular oil changes, fluid top-ups, and manufacturer-recommended repairs-signals that the engine and transmission received proper care. Conversely, a vehicle with no service records and suddenly appears on the market after years of silence raises serious red flags about what happened during that gap.

The National Vehicle Title Information System (NMVTIS) aggregates the most critical data from state motor vehicle agencies and law enforcement, making it the official federal resource for vehicle history. Data in these reports comes directly from official sources required by federal law to report regularly, so you work with documented facts rather than seller honesty or guesswork.

Title Problems Signal Deeper Issues

Title problems carry equal weight to accident history. Vehicles branded as salvage, flood-damaged, or lemon have significantly lower value and carry hidden risks that affect safety and reliability. A flood-damaged car may function temporarily but will develop electrical and mechanical failures that prove costly and dangerous.

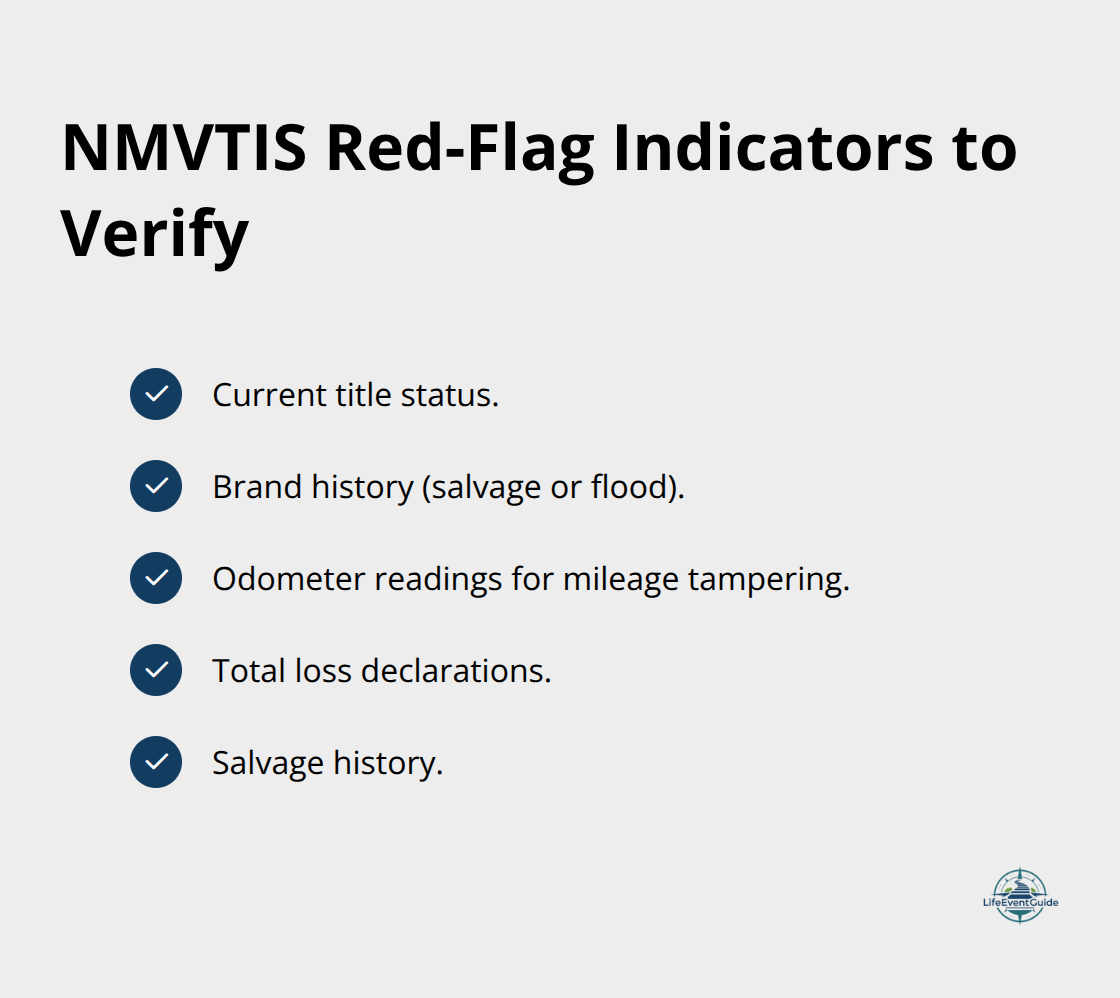

NMVTIS tracks specific indicators to prevent fraud: current title status, brand history (salvage or flood), odometer readings (to catch mileage tampering), total loss declarations, and salvage history. If any of these flags appear on a report, the vehicle’s structural integrity and safety are genuinely compromised. These indicators exist because they reveal the problems most likely to cause expensive failures or safety hazards after you drive off the lot.

Understanding what these reports contain prepares you to spot the red flags that matter most. The next section walks you through exactly what to look for when you open that report.

What to Look For in a Vehicle History Report

Accident History and Damage Severity

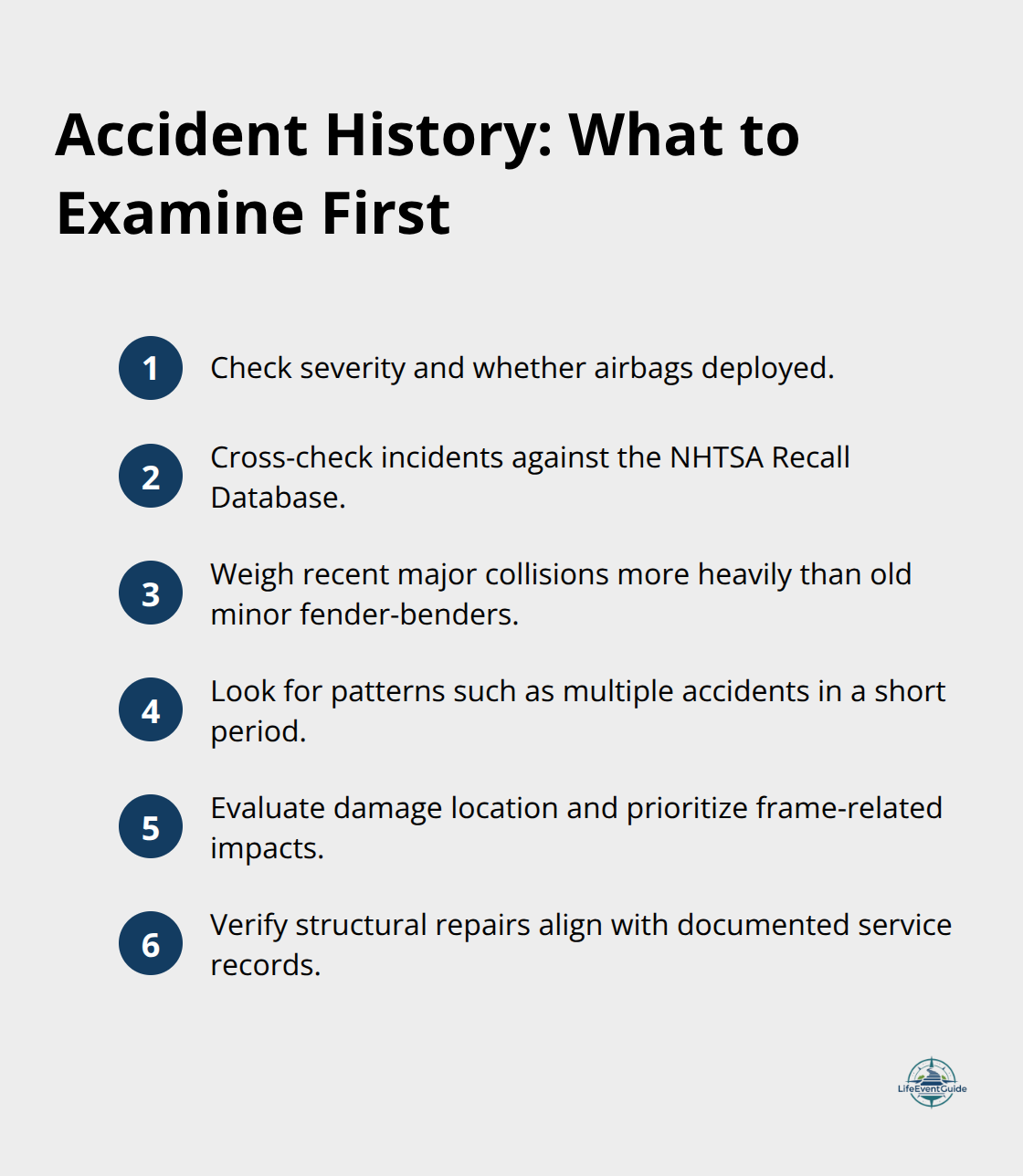

Accident reports on a vehicle history report show severity, date, location, and whether airbags deployed-this detail matters because airbag deployment signals a collision serious enough to trigger safety systems. Cross-check any accident against the NHTSA Recall Database to understand if that specific vehicle model had known issues during that time period. A minor fender-bender from five years ago carries far less weight than a major collision from last month, but both tell you something different about the car’s past.

Look for patterns in the accident history. A single accident might reflect bad luck, but three accidents in four years suggests either poor driving or unreported structural damage that keeps getting hit. The location of damage matters significantly-frame damage to the front or rear affects how the vehicle absorbs impact, while side-panel damage poses less structural risk. If the report shows structural repairs without matching service records, that’s a red flag that work occurred off-the-books or by an unqualified shop.

Title Status and Ownership Patterns

A clean title means no brands like salvage, flood, or lemon; any brand significantly lowers value and indicates the vehicle experienced major damage or defect. Flood-damaged vehicles warrant extra scrutiny because water damage causes hidden electrical and mechanical failures that emerge months later-look for inconsistencies in controls and brittle wiring that indicate corrosion inside components you cannot see during inspection.

The number of previous owners and how long each held the vehicle tells you about usage patterns. A car with five owners in three years suggests problems that drove people away, while one owner over eight years suggests stability. Verify that the VIN matches across all documents (title, registration, insurance, and service receipts) to avoid title or documentation fraud.

Mileage Consistency and Service Records

Mileage consistency across all records is non-negotiable: if the odometer reading jumped backward or showed massive gaps between reports, odometer fraud occurred. Service records from authorized dealerships carry more weight than independent shops because they include factory-documented maintenance. A vehicle missing service records during critical intervals-like skipping a timing belt replacement at 100,000 miles-predicts expensive future failures.

Compare reported maintenance against the manufacturer’s recommended schedule to spot what was neglected. Factor those future repairs into your offer price. Service history reveals whether the previous owner actually maintained the vehicle or ignored it; a complete record signals that the engine and transmission received proper care, while gaps raise serious red flags about what happened during those periods.

With these specific details in mind, you now know what information matters most on a report. The next step involves using multiple reports to compare vehicles and make a confident purchasing decision.

How to Use Vehicle History Reports in Your Buying Decision

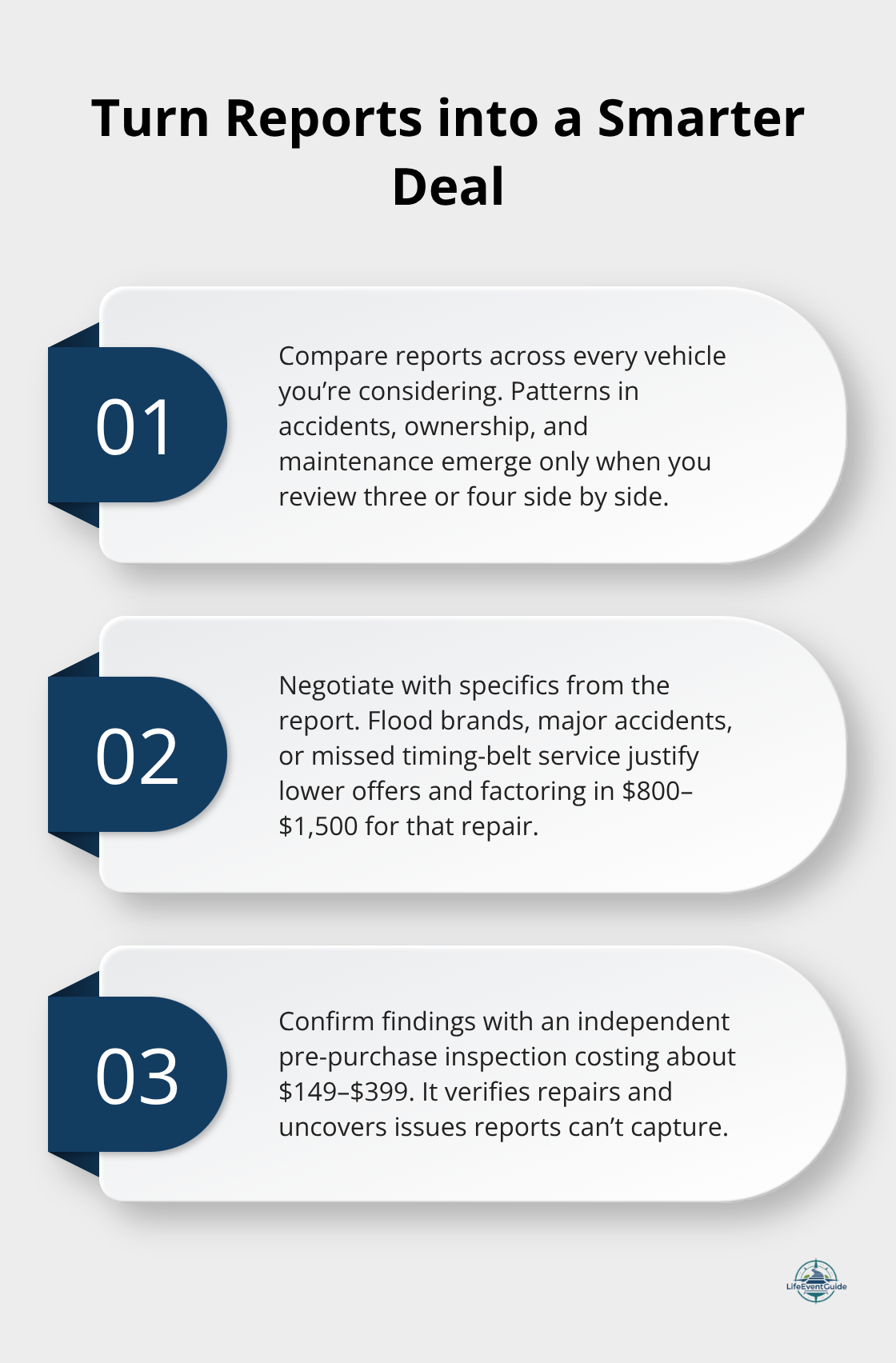

Compare Reports Across Multiple Vehicles

Vehicle history reports become truly powerful when you stop treating them as standalone documents and start using them as negotiation tools. Pull reports on every vehicle you seriously consider, not just your top choice. When you compare three or four reports side by side, patterns emerge that single reports hide. A car with one minor accident five years ago sits in a completely different category than an identical model with two accidents in the past year.

Carfax charges around $45 per report while AutoCheck runs about $30, so spending $90 to $180 comparing vehicles before you negotiate saves far more than that in overpriced offers. Line up the reports chronologically and note which vehicle shows the cleanest service intervals, fewest ownership changes, and most recent maintenance. That comparison instantly tells you which car represents actual value and which one carries hidden risk masked by a low asking price.

Negotiate Price Based on Report Findings

Use report findings as concrete leverage during price negotiations. A vehicle with a reported major accident should cost significantly less than an identical model with a clean history, yet many sellers price them identically and hope buyers don’t check. If the report shows a flood brand, the vehicle’s value drops significantly compared to an unmarked equivalent.

If service records show a missed timing belt replacement at the manufacturer’s recommended interval, factor the $800 to $1,500 replacement cost directly into your offer. Sellers who provide their own report upfront signal confidence in the vehicle’s condition, while those who resist or delay often know something problematic exists. Before you test drive a single car, obtain reports on your shortlist and use the findings to eliminate vehicles that don’t justify their asking prices.

Combine Reports with In-Person Inspection

After narrowing to your final choice, schedule an independent pre-purchase inspection from a certified mechanic, which typically costs $149 to $399 depending on scope. That inspection verifies what the report claims and catches mechanical issues that reports cannot capture. A mechanic can confirm whether accident repairs were completed properly, whether rust or corrosion indicates hidden water damage, and whether the vehicle’s current condition matches its reported history.

Never skip this step regardless of how clean the report appears. The report provides documented history, but only a hands-on inspection reveals the vehicle’s actual mechanical state and safety condition. Document everything before you finalize your purchase to protect yourself from purchasing a vehicle that looks good on paper but fails in reality.

Final Thoughts

Vehicle history reports transform used car buying from guesswork into a systematic process that protects your investment. A vehicle history report checklist ensures you examine accident severity and patterns, title brands that signal major damage, mileage consistency across all records, and service gaps that predict future repairs. These details separate vehicles worth buying from those that will drain your wallet in unexpected repairs.

Pull reports on every vehicle you seriously consider, compare them side by side, and use the findings to negotiate fair prices (reports cost $25 to $45 each, far less than the thousands hidden damage costs after purchase). Schedule an independent pre-purchase inspection from a certified mechanic for $149 to $399 to verify what the report claims and catch mechanical issues that reports cannot capture. This combination of documented history and hands-on assessment protects you from purchasing a vehicle that looks good on paper but fails in reality.

At LifeEventGuide, we help you navigate major life transitions with clear planning and systematic decision-making. Visit our resources to access checklists and frameworks that guide you through vehicle purchases and other significant life events while helping you avoid common mistakes.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.