I learned the hard way that buying a home is just the beginning of your financial commitment.

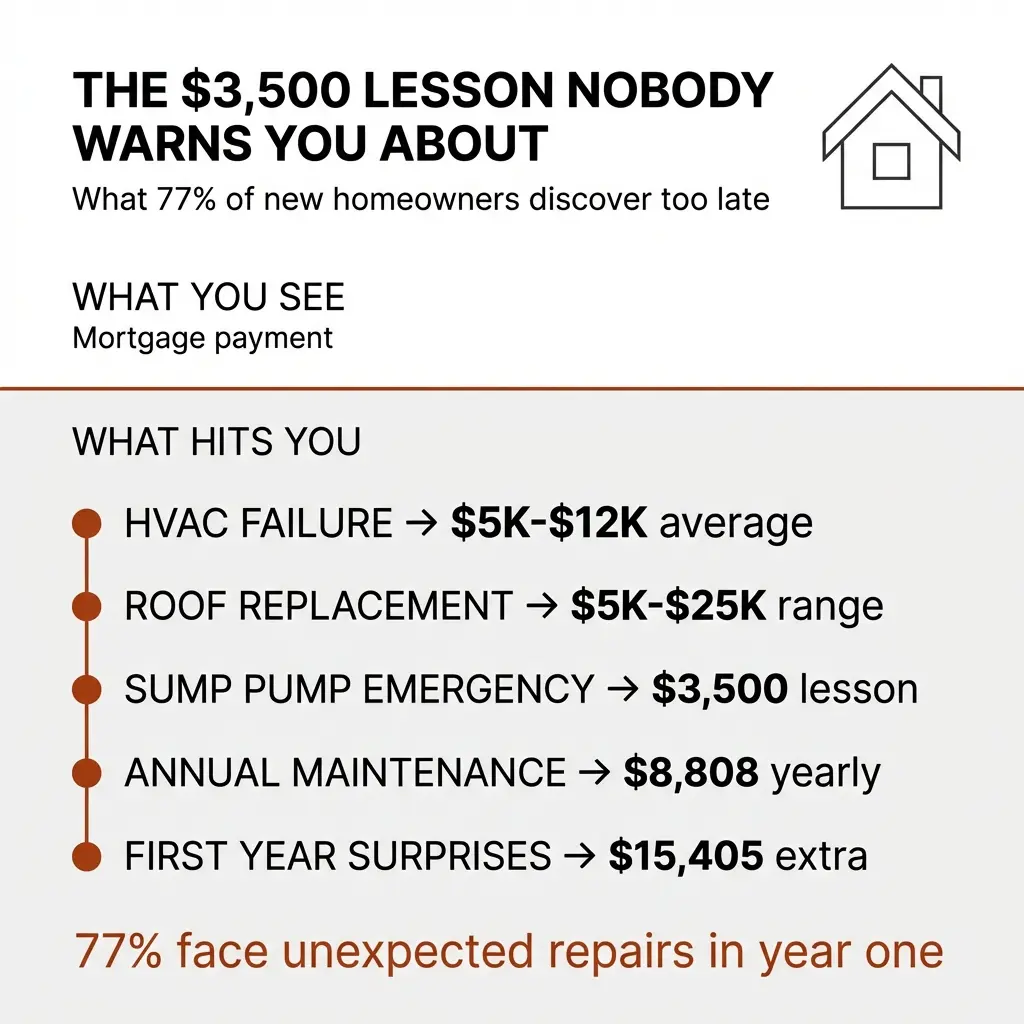

Everyone talks about down payments and mortgage rates. Nobody mentions the $3,500 sump pump replacement two months after closing.

Or the air conditioning unit that dies a year later.

These weren’t small inconveniences. They were financial gut punches that standard home-buying advice never prepared me for. And I’m not alone—77% of homeowners face unexpected repair costs in their first year of ownership.

The Financial Blind Spot Everyone Has

When I started assessing my finances for home buying, I did everything right.

I checked my credit score. I calculated my debt-to-income ratio. I used mortgage calculators to estimate monthly payments including property taxes and insurance.

But here’s what those calculators don’t tell you: home maintenance accounts for an average of $8,808 annually. That’s on top of your mortgage, taxes, and insurance.

The real kicker? 52% of homeowners admit the true cost of owning a home surprised them, with the average homeowner shelling out an additional $15,405 each year beyond their mortgage payment.

I wish someone had told me to budget 1% to 4% of my home’s value annually just for maintenance. Instead, I learned this lesson when my sump pump failed just two months after I bought my first house.

The $3,500 Wake-Up Call

Two months into homeownership, my basement started flooding.

The sump pump had failed completely. The replacement cost me $3,500—money I didn’t have budgeted because I’d just depleted my savings on the down payment and closing costs.

This wasn’t an unusual situation. The average sump pump replacement ranges from $644 to $2,105, but costs can climb to $4,700 depending on the system complexity. Mine was on the higher end because of how the previous system was installed.

A year later, in a different house, my air conditioning unit died. HVAC replacement in 2025 ranges from $5,000 to $12,000, with most homeowners paying around $13,430 for a complete system.

These experiences changed how I approach home buying entirely.

What I Now Know About Home Inspections

After getting burned twice, I realized the problem wasn’t just maintenance costs.

The problem was my home inspector.

Here’s something most first-time buyers don’t know: over 1 in 4 homeowners ended up discovering something in their homes that their inspector should have found. Additionally, 13% regret using the home inspector they did, and 27% wish their inspector had been more thorough.

I learned this lesson backwards. When I sold one of my houses, the buyer’s inspector was incredibly thorough. He found things my original inspector had completely missed.

Things a Tough Inspector Catches

The buyer’s inspector found fogging between glass panels in the windows—a sign of seal failure that would eventually require replacement.

He noticed electrical outlets installed upside down, which isn’t just an aesthetic issue but can indicate rushed or improper electrical work throughout the house.

He spent time examining the HVAC system’s age and condition, not just whether it was currently working.

That experience taught me more about home inspections than my own purchases ever did.

How to Find a Really Tough Inspector

Most people ask their real estate agent for an inspector referral.

This creates a conflict of interest you need to understand. Your agent wants to close the deal. An inspector who finds too many problems can kill deals. An inspector who gets referrals from agents may feel pressure to go easy on inspections.

Consumer experts advise: unless you deeply trust your agent, find your own inspector.

Now when I buy a house, I look for inspectors with specific characteristics. I want someone who has been doing this for at least 10 years. I read reviews looking for complaints that they’re “too picky” or “found too many minor issues”—those are actually positive signs.

I also make sure I’m present during the inspection. Being there in person has taught me more than any written report ever could.

What Being Present During Inspection Reveals

When you’re physically there, you see how the inspector approaches each system.

You can ask questions in real-time. You can see their facial expressions when they find something concerning. You can watch them test things multiple times if they’re not satisfied with the first result.

The written report will tell you there’s a problem. Being present tells you how serious the inspector thinks it really is.

If I’m not satisfied with the first inspection, I’ll get a second one done. Yes, it costs more money upfront. But it’s nothing compared to a $3,500 surprise two months after closing.

The Big-Ticket Items You Need to Examine

I now focus obsessively on anything that could be a major expense if it breaks.

This means going beyond the standard inspection checklist.

HVAC System

Ask how old the system is. Ask when it was last serviced. Ask to see maintenance records if the seller has them.

Most HVAC systems last 15-20 years. If the system is 12 years old, you need to budget for replacement soon—even if it’s currently working fine.

Roof

Get the age of the roof in writing. Ask about the warranty. Look for signs of patch jobs that might indicate recurring problems.

A roof replacement can cost $5,000 to $25,000 depending on size and materials.

Water Heater

These typically last 8-12 years. If it’s older than 8 years, replacement should be in your near-term budget.

Foundation and Drainage

This is where my sump pump lesson comes in. Ask about basement flooding history. Ask neighbors if you can. Look for water stains or musty smells.

Foundation repairs can cost thousands or even tens of thousands of dollars.

Plumbing

Old pipes can mean constant leaks and eventual full replacement. Ask about the age of the plumbing system and what material the pipes are made from.

The First Year Reality Check

Even with perfect inspections, you need to prepare for the first year.

The average homeowner encounters about four surprises or unexpected costs within the first year, spending around $3,600 to address them. Top expenses include appliance replacement (56%), exterior repairs like windows (53%), and major repairs like roofing (52%).

Here’s what nobody tells you: 44% of homeowners experienced their first surprise repair within the first year after closing, and 12% faced one in the first month.

You need an emergency fund specifically for home maintenance. I recommend having at least $5,000 to $10,000 set aside beyond your regular emergency savings.

What About Pre-Approval and Financing?

Getting pre-approved is important, but it’s not just about knowing how much you can borrow.

It’s about understanding what you’re committing to for the next 15 to 30 years.

When you get pre-approved, lenders tell you the maximum you can borrow. This is almost always more than you should actually spend. Lenders don’t factor in your lifestyle, your other financial goals, or those maintenance costs we’ve been discussing.

I learned to take the pre-approval amount and reduce it by 20-25%. That gives you breathing room for maintenance, repairs, and life.

Shop Around for Lenders

Don’t just go with the first lender your agent recommends.

Talk to local banks, credit unions, and online lenders. Compare not just interest rates but also fees, closing costs, and loan terms.

A difference of even 0.25% in interest rate can save you thousands over the life of the loan.

The Real Estate Agent Question

Your agent works for you, but they also work on commission.

They get paid when the deal closes. This creates an incentive structure you need to understand.

A good agent will prioritize your long-term satisfaction over closing one specific deal. They’ll encourage you to walk away from a house with too many problems. They’ll support getting multiple inspections if needed.

A mediocre agent will push you toward closing because that’s how they get paid.

Ask potential agents: “Tell me about a time you advised a client not to buy a house.” Their answer will tell you everything you need to know.

House Hunting Without Losing Your Mind

House hunting is emotionally exhausting.

You’ll fall in love with houses that are overpriced. You’ll find perfect houses that go under contract before you can make an offer. You’ll attend dozens of open houses that all start to blur together.

Here’s what helped me: I created a spreadsheet with every house I viewed. I noted the address, price, pros, cons, and big-ticket items that would need replacement soon.

This removed some of the emotion from the process. When I looked back at my notes, I could see patterns I’d missed in the moment.

I also learned to separate “want” from “need.” That beautiful kitchen is nice, but it doesn’t matter if the roof needs replacing in two years.

Making an Offer That Protects You

When you make an offer, contingencies are your protection.

Never waive the inspection contingency. Nearly 1 in 4 homeowners waived their home inspection before purchase, and 23% regretted it while 41% said it didn’t save them money in the long run.

The inspection contingency lets you walk away or renegotiate if major problems are found.

The financing contingency protects you if your loan falls through.

The appraisal contingency matters if the house appraises for less than your offer price.

Yes, waiving contingencies can make your offer more competitive. But it also removes your safety net. In my experience, it’s not worth the risk.

What Closing Day Actually Looks Like

Closing day involves signing more documents than you thought possible.

Review everything carefully. Understand every fee. Ask questions about anything that looks different from what you expected.

Bring a certified check or arrange a wire transfer for your down payment and closing costs. These typically range from 2% to 5% of the home’s purchase price.

Adding up down payment, furnishing, renovations, and tools purchased, the first year of homeownership can cost $86,698. Nearly 1 in 4 people didn’t budget for closing fees at all.

Once everything is signed and the money is transferred, you get the keys.

That moment feels incredible. Just remember that homeownership is a marathon, not a sprint.

What I Wish Someone Had Told Me

Buying a home is exciting. It’s also the largest financial commitment most people ever make.

The standard advice focuses on credit scores, down payments, and mortgage rates. That’s important, but it’s incomplete.

The real cost of homeownership includes maintenance, repairs, and unexpected failures. Budget for these from day one.

Find the toughest inspector you can, not the nicest one. Be present during the inspection. Don’t be afraid to get a second inspection if something feels off.

Examine big-ticket items obsessively. Know the age and condition of every major system in the house.

Take your pre-approval amount and reduce it by 20-25% to find what you should actually spend.

Understand that your agent, your lender, and even your inspector all have incentive structures that may not perfectly align with your long-term interests.

Keep detailed notes during house hunting to remove emotion from your decision-making.

Never waive contingencies just to make your offer more competitive.

And most importantly: expect surprises in the first year. Budget for them. Prepare for them.

Because that $3,500 sump pump replacement taught me more about homeownership than any guide ever could.

The excitement of getting the keys is real. Just make sure you’re financially prepared for everything that comes after.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.