Buying a home is one of the biggest financial decisions you’ll make, and it’s easy to feel overwhelmed by the numbers. We at LifeEventGuide know that having a clear home buying budget checklist helps you stay confident and in control throughout the process.

This guide walks you through calculating what you can afford, understanding the real costs involved, and tracking your finances every step of the way.

Know Your Financial Foundation Before House Hunting

Calculate What You Can Put Down

Before you determine what price range makes sense, you need an honest picture of where you stand financially. List everything in your savings account and calculate how much you can realistically put toward a down payment.

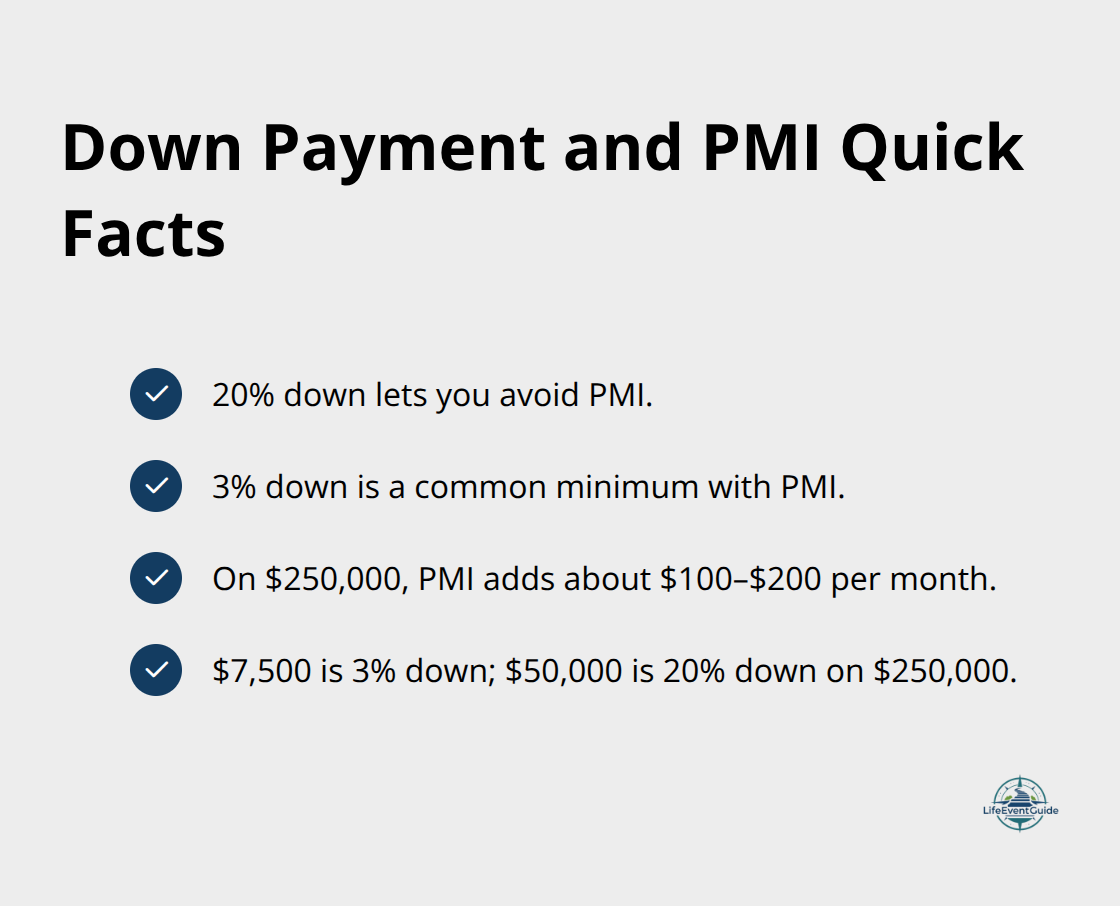

The standard advice says to try for 20% down to avoid private mortgage insurance, but that’s not realistic for everyone. A 3% down payment is the minimum many lenders accept, though it triggers PMI costs that add roughly $100–$200 monthly to your mortgage on a $250,000 home.

If you have $7,500 saved for a $250,000 purchase, that’s only 3% down. If you have $50,000 saved, you hit the 20% threshold and skip PMI entirely. The difference between these two scenarios means paying thousands more in PMI over time, so knowing your exact savings number forces you to make a real choice about what you can afford right now versus what you might afford later.

Understand How Your Credit Score Affects Your Rate

Your credit score can help you qualify for a lower interest rate, and even small rate differences compound into tens of thousands of dollars over 30 years. A borrower with a 760+ credit score might qualify for a 6.2% rate, while someone with a 620 score could face 7.8% on the same loan amount. On a $200,000 mortgage, that 1.6% difference means roughly $200 more per month.

If your credit score is below 700, seriously consider spending the next few months paying down debt and disputing any errors on your credit report before applying for a mortgage. This step alone can save you significant money over the life of your loan.

Calculate Your Debt-to-Income Ratio

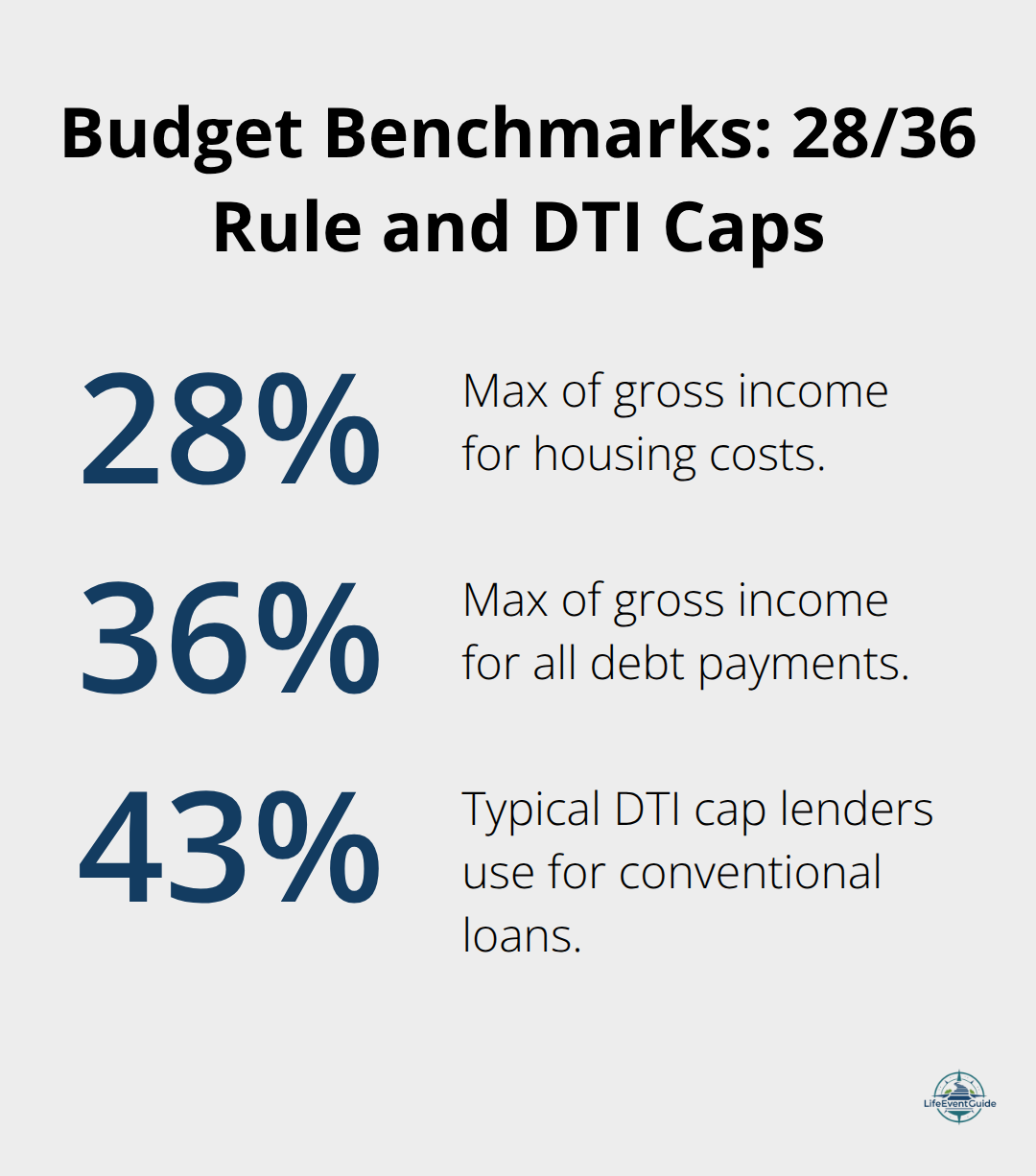

Your debt-to-income ratio tells lenders what percentage of your gross monthly income goes toward existing debts plus the new mortgage payment. Most lenders cap this at 43% of gross income for conventional loans, though some FHA loans allow different ratios. If you earn $7,500 monthly and already pay $1,500 toward a car loan and student loans, you have $3,225 left for a mortgage payment (43% of $7,500).

That $3,225 monthly payment translates to roughly a $550,000 loan, but property taxes, insurance, and PMI will consume part of that budget, shrinking your actual home price. Calculate your current debts honestly, subtract them from 43% of your gross income, and you’ll know exactly how much mortgage payment you can handle without lenders rejecting you. With these three numbers in place-your down payment savings, your credit score, and your debt-to-income capacity-you’re ready to determine what price range actually works for your situation.

What Price Range Can You Actually Afford

Apply the 28/36 Rule to Your Situation

The 28/36 rule gives you a straightforward way to find your maximum affordable price, though the math requires honesty about your actual monthly obligations. Take your gross monthly income and multiply it by 0.28 to find the maximum you should spend on housing costs alone (mortgage, property taxes, insurance, and PMI). If you earn $7,500 monthly, that’s $2,100. Multiply your gross income by 0.36 to find the absolute ceiling for all debt payments combined, which gives you $2,700.

This second number matters because lenders will reject you if your total monthly obligations-car loans, student debt, credit cards, plus the new mortgage-exceed 43% of gross income on conventional loans.

Calculate What Your Debt Leaves for a Mortgage

Start with your current monthly debt payments. If you’re paying $400 toward a car loan and $300 toward student loans, you have $2,000 left for your mortgage before hitting the 36% threshold. That $2,000 payment on a current mortgage rate of around 6.5% translates to roughly a $300,000 loan, but closing costs, property taxes, and insurance will reduce what you can actually spend on the home itself.

Account for the Hidden Housing Costs

The real trap is treating the mortgage payment as your only housing cost. Property taxes vary wildly by location, so a $250,000 home costs far less monthly in Pittsburgh than in Memphis. Homeowners insurance typically runs about $35 monthly for every $100,000 of home value, meaning a $300,000 home adds roughly $105 to your monthly payment. If you put down less than 20%, PMI adds another $100–$200 monthly depending on your loan size.

Factor in HOA Fees and Local Variations

HOA fees, which can range from $100 to $500+ monthly in some communities, must come out of that 28% housing budget, not be added on top. Calculate your actual property tax rate by checking your county assessor’s website, get a homeowners insurance quote from at least two providers, and confirm whether the neighborhood has HOA fees before deciding on a price range. A $300,000 home in one area might consume 32% of your income while the same payment in another area hits 38% once you factor in taxes and insurance. The difference between staying comfortably within your budget and stretching too far often comes down to these three costs, not the mortgage payment alone. With your actual price range now defined by local expenses and your debt capacity, you’re ready to track every cost that appears between now and closing day.

Tracking Costs Before You Close

List Every Expense from Offer to Closing

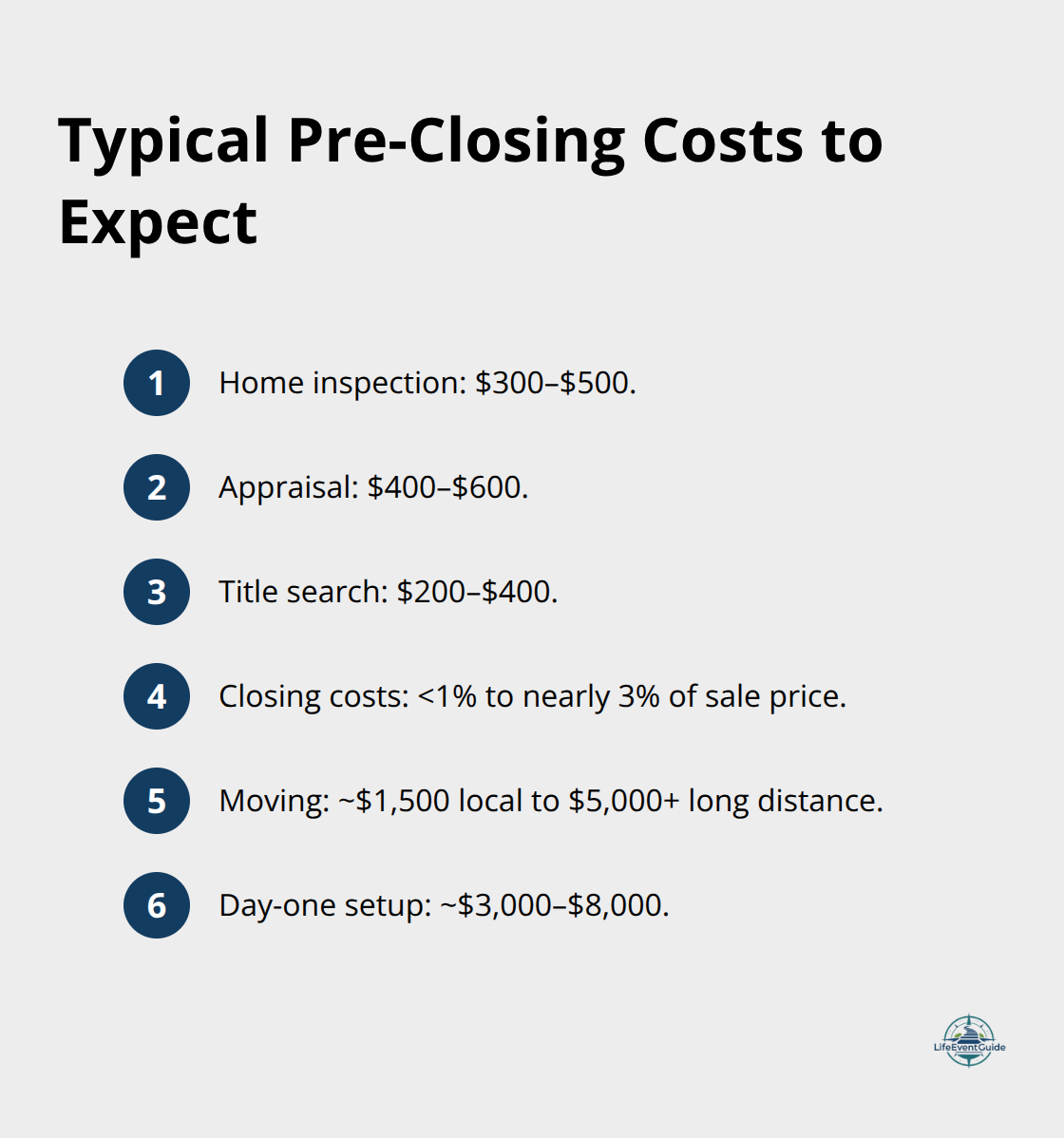

The home buying process generates expenses long before you sign final paperwork, and most buyers underestimate how much they’ll spend between making an offer and closing day. A home inspection costs $300–$500, an appraisal runs $400–$600, and title search fees add another $200–$400.

Closing costs can range from less than 1 percent to nearly 3 percent of your home’s sale price, meaning a $300,000 home triggers significant lender fees, title insurance, appraisal, and attorney costs. Beyond these predictable expenses, you’ll face moving costs ranging from $1,500 for a local move to $5,000+ for long distance, plus immediate home needs like furniture, paint, and appliance replacements.

Create a spreadsheet right now and list every expense you’ve already paid toward this purchase. Add inspection, appraisal, and closing cost estimates based on your target price range. Then add realistic moving costs and first-month home setup expenses. Most buyers report spending $3,000–$8,000 on these day-one costs alone, so this isn’t theoretical padding-it’s money that leaves your account before you ever make a mortgage payment.

Separate Your Down Payment from Closing Costs

Your approved mortgage amount doesn’t account for the actual cash you need on hand at closing. Your lender might approve you for a $300,000 loan, but if you’ve exhausted your savings on the down payment with nothing left for closing costs and moving, you’ll either lose the home or take on debt right when you’re taking on a mortgage. Set aside closing costs separately from your down payment funds starting today.

If you’re putting 5% down on a $250,000 home, that’s $12,500, plus roughly $5,000–$12,500 in closing costs, plus $3,000–$5,000 in moving and setup. You need at least $20,500–$30,000 liquid before you make an offer, not just the down payment amount. Once you’re in contract, expenses accelerate. The inspector finds issues, the appraisal might come in low forcing renegotiation, and the title search uncovers problems that cost money to resolve.

Plan for Unexpected Costs and Final Verification

Stop assuming your budget is locked in once you’re approved. Instead, plan for 10–15% in additional expenses beyond your closing cost estimate, and keep that buffer in a separate savings account untouched until you close. Two weeks before closing, your lender will provide a Closing Disclosure statement showing your exact final costs.

Compare this line-by-line against your initial estimate and your budget. If costs have climbed beyond what you anticipated, you still have time to ask your lender for clarification or negotiate with the seller to cover certain fees (inspection repairs, title issues, or appraisal shortfalls). Never sign closing documents without understanding every charge, and never proceed if the final numbers push you into financial strain.

Final Thoughts

Your home buying budget checklist now contains every number that matters: your down payment savings, your debt-to-income ratio, your maximum monthly payment, and all costs between now and closing day. Pull out your spreadsheet and compare what you planned against what actually occurs in your situation. If your credit score improved since you started, you might qualify for a better rate, but if unexpected expenses drained your savings, you may need to adjust your price range downward or delay your purchase.

The next steps depend on where you stand financially right now. If your numbers are solid and your finances are stable, move forward with getting pre-approved by a lender-this transforms your budget from theory into a concrete loan amount that sellers will take seriously. If gaps exist between your budget and your financial reality, address them now rather than during closing (pay down high-interest debt, boost your credit score, or save longer for a larger down payment).

Keep your home buying budget checklist accessible throughout the entire process and reference it when you’re tempted to stretch beyond your price range or when unexpected costs appear. We at LifeEventGuide understand that major life transitions like buying a home require more than just a budget-they need a complete framework to guide you through every decision, and our event-specific checklists and playbooks help you avoid common mistakes and complete this transition calmly.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.