Buying a home is one of the biggest financial decisions you’ll make, and the mortgage options available can feel overwhelming. At LifeEventGuide, we’ve created this financing options checklist to help you understand what’s out there and make a choice that fits your situation.

The right mortgage depends on your budget, timeline, and comfort with risk. This guide walks you through the main types of mortgages, how to compare costs, and the steps to pick the best option for you.

What Mortgage Types Should You Consider

Fixed-rate mortgages lock your interest rate for the entire loan term, typically 15 or 30 years. Your monthly payment stays the same from day one to the final payment. The stability of fixed-rate mortgages makes them predictable for budgeting, which is why most homebuyers choose this option. You know exactly what you’ll pay each month, so you can plan your finances around your mortgage with confidence. The trade-off is that fixed rates are typically higher than the initial rates on adjustable-rate mortgages, so you pay for that certainty upfront.

When adjustable rates make sense

Adjustable-rate mortgages start with a lower initial rate that increases after a set period, usually 3, 5, 7, or 10 years. If you plan to sell or refinance before the rate adjusts, an ARM can save you thousands in interest during those early years. This option works best if you’re confident about your timeline and comfortable with the risk that rates could rise significantly. Many first-time buyers avoid ARMs because the uncertainty feels risky, but if your situation is temporary, the math often favors this choice. The CFPB recommends understanding exactly how your payment will change over time before you commit to an ARM, since some borrowers face payment increases of several hundred dollars monthly when rates adjust.

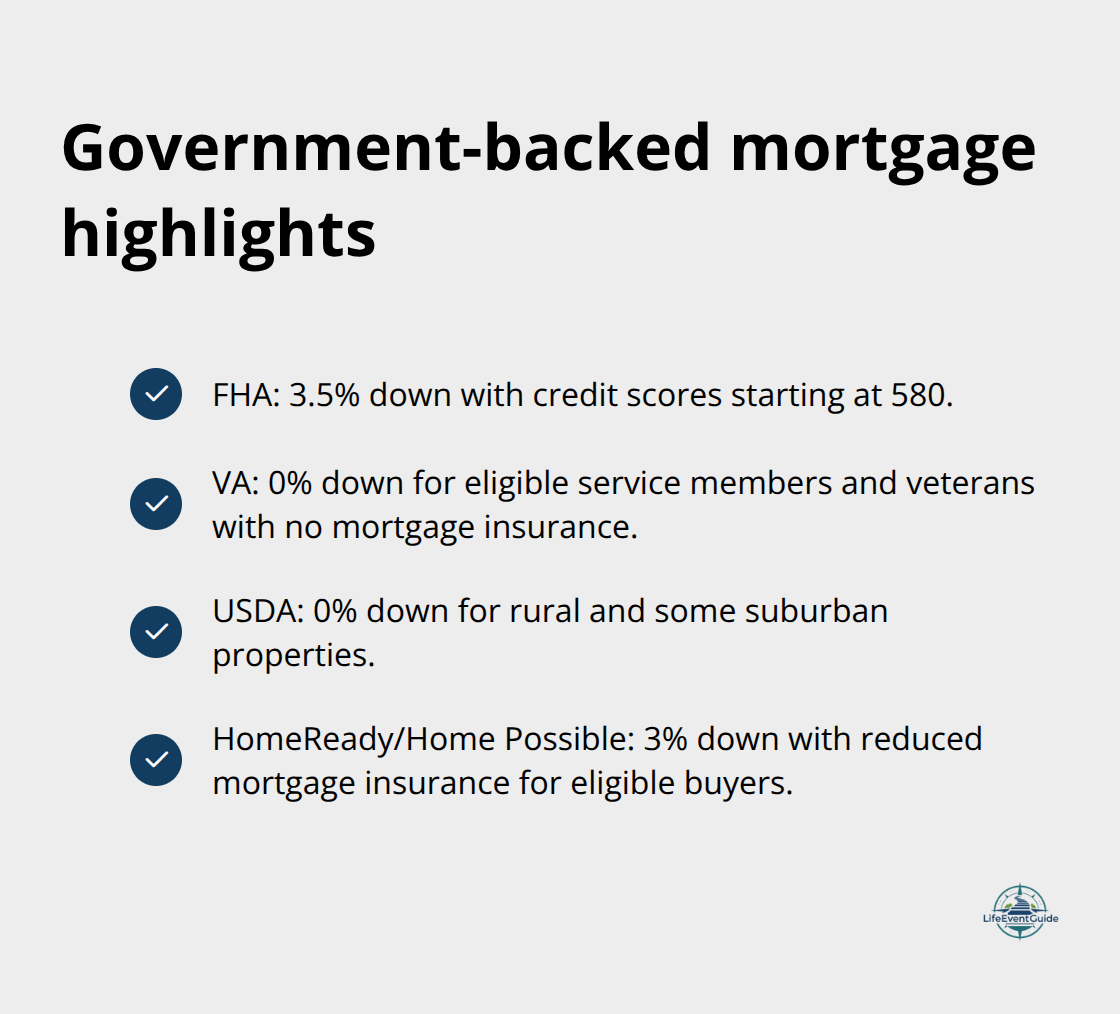

Government-backed programs for qualified buyers

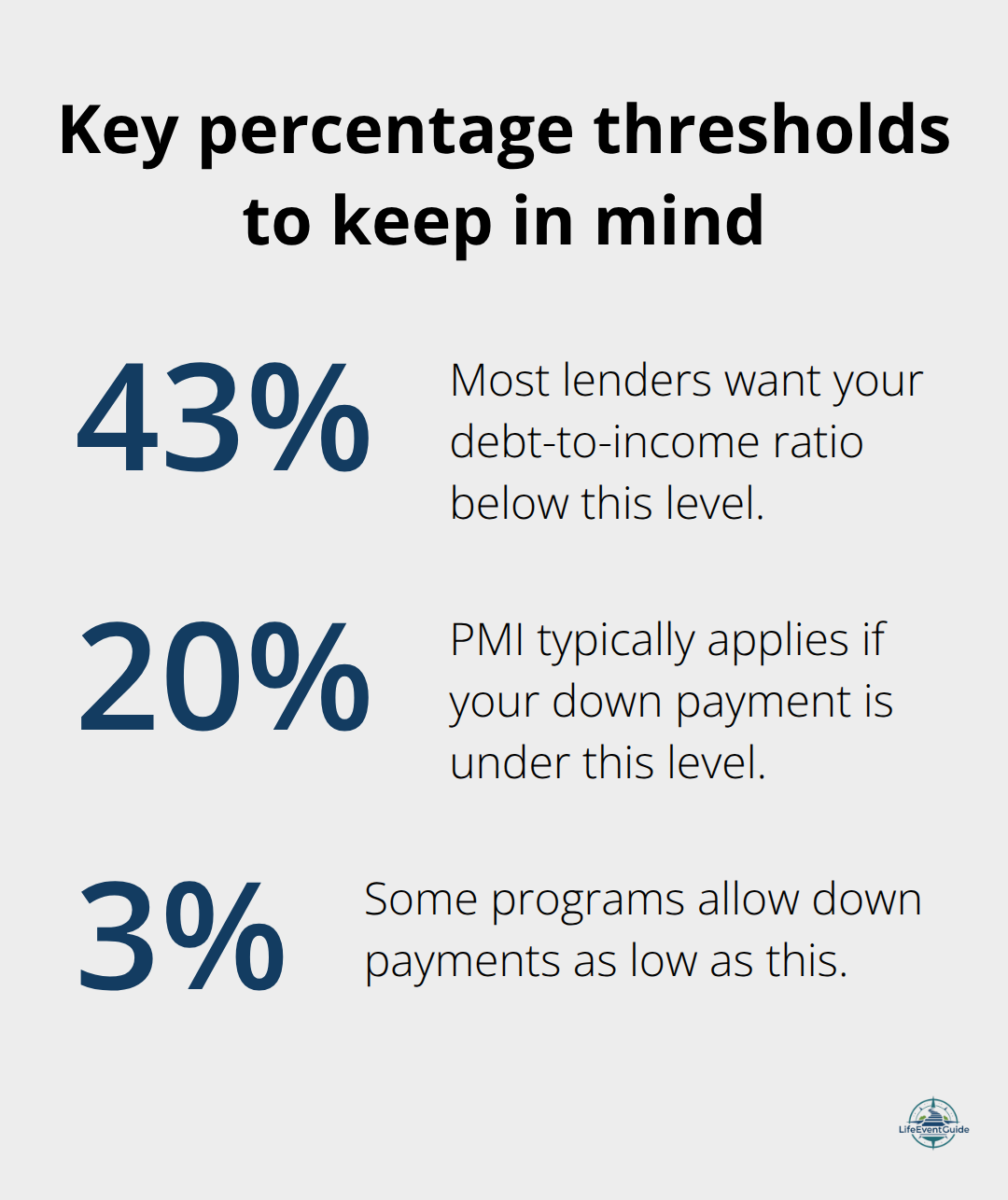

Federal Housing Administration loans allow down payments as low as 3.5% with credit scores starting at 580, according to FHA guidelines. VA loans offer 0% down for eligible service members and veterans with no mortgage insurance requirement. USDA loans provide 0% down financing for rural and suburban properties, often with lower interest rates than conventional options. Fannie Mae’s HomeReady and Freddie Mac’s Home Possible programs target low-to-moderate income buyers with 3% down and reduced mortgage insurance costs (each program has specific eligibility requirements and features). Comparing these programs against conventional mortgages reveals which option saves you the most money based on your circumstances.

The next step is to understand how these different mortgage types affect your actual costs and monthly payments.

What Actually Costs More When Comparing Mortgages

Interest rates tell only half the story

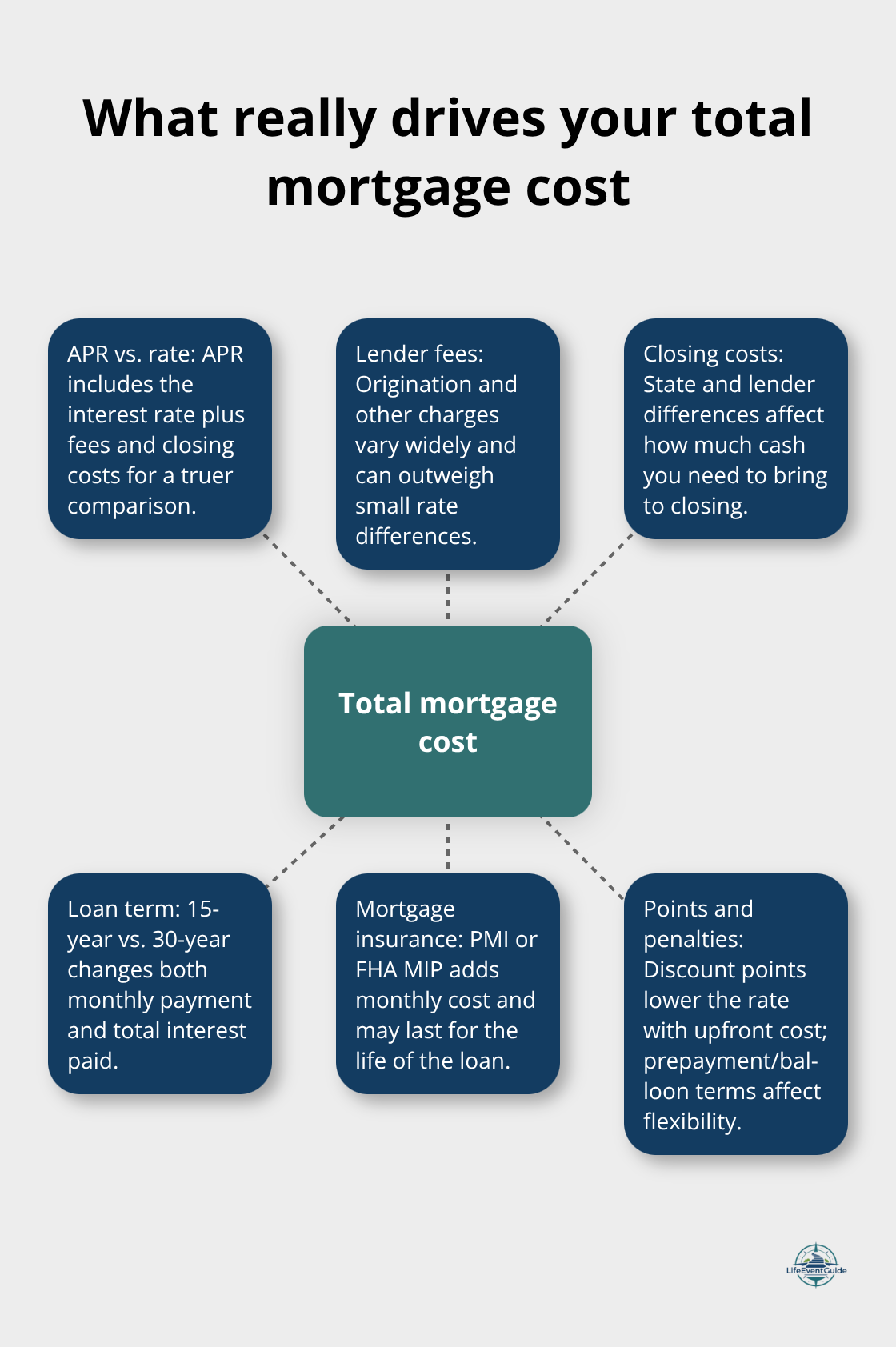

Interest rates grab all the attention, but they’re only part of the picture. The CFPB recommends you obtain at least three loan estimates from different lenders so you can see the full cost breakdown, not just the rate. When you compare offers, look at the APR instead of the interest rate alone-APR includes the rate plus fees and closing costs, which gives you a more honest comparison of total borrowing cost. A lender advertising 6.5% might charge $3,000 in fees, while another at 6.75% charges $500. Over a 30-year loan, that rate difference saves roughly $72,000 according to CFPB data, but you need to subtract the fee difference to see which lender actually costs less.

Closing costs and upfront expenses

Closing costs can vary significantly by state, ranging from less than 1 percent of the home’s sale price to nearly 3 percent, so on a $300,000 home, you should expect $3,000 to $9,000 upfront. The estimated cash to close shows exactly how much money you need to bring to closing day, not just your monthly payment. Compare this figure across multiple lenders to understand your true upfront cost. This comparison reveals which lender fits your financial situation best.

How loan terms reshape your total cost

A 15-year mortgage has higher monthly payments but costs far less in interest over time compared to a 30-year loan on the same amount. The 30-year fixed remains standard for most 3% down programs like Conventional 97, HomeReady, and Home Possible because it keeps monthly payments manageable. When you review loan documents, check for prepayment penalties (which prevent you from paying off the loan early without a fee) and balloon payments (which require a large lump sum at the end). Discount points let you lower your interest rate by paying upfront-each mortgage point typically lowers your loan’s interest rate by 0.25 percentage points for the life of the loan, so calculate your break-even point to decide if paying points makes sense for your timeline.

Mortgage insurance and program differences

Private mortgage insurance adds to your monthly cost when your down payment is under 20%, but different programs handle it differently. FHA requires mortgage insurance premiums for the life of the loan, while HomeReady and Home Possible offer reduced PMI for eligible borrowers, which makes a real difference in long-term cost. You should also shop across lender types: national banks, regional banks, credit unions, and mortgage companies all offer different fee structures and product menus. Some credit unions provide better rates or lower costs for their members, so don’t overlook this option.

Where to find the best rates and terms

National banks, regional banks, credit unions, and mortgage companies each bring different advantages to the table. You can compare current offers using online rate tables and calculators to estimate long-term costs across different scenarios. Ask lenders for a detailed breakdown of closing costs and fees, and don’t hesitate to negotiate terms or costs when possible. The next step is to assess your own financial situation and determine which mortgage option aligns with your budget and timeline.

How to Pick Your Mortgage Without Getting Lost in the Details

Assess your financial situation first

Know exactly what you can afford before you talk to a single lender. Pull together your recent tax returns, W-2s, bank statements, and a list of all your debts-credit cards, student loans, car payments, everything. Lenders will ask for these documents anyway, so gathering them now speeds up the process and forces you to see your full financial picture. Calculate your debt-to-income ratio by dividing your monthly debt payments by your gross monthly income. Most lenders want this ratio below 43%, meaning if you earn $5,000 monthly, your total monthly debt shouldn’t exceed $2,150.

This number matters more than how much a lender says you can borrow. Set your maximum mortgage payment based on what actually fits your lifestyle, not what a lender approves. If you can comfortably afford $1,500 monthly but a lender approves you for $2,200, stick with $1,500.

Obtain multiple loan estimates strategically

The CFPB recommends obtaining at least three loan estimates from different lenders, and the 14- to 45-day window for rate shopping means multiple credit inquiries during this period won’t significantly damage your credit score. Spread your applications across this timeframe rather than submitting them all at once. Request loan estimates in writing from each lender, and they must provide the same standardized form so you can compare apples to apples.

Compare what actually matters on each estimate

Ignore the interest rate and focus on the APR versus interest rate and total estimated cash to close instead. The APR reveals what you actually pay when fees are included, while cash to close shows your upfront burden. A lender offering 6.5% with $2,000 in fees costs less than 6.3% with $5,000 in fees if you’re keeping the loan long-term. Look for prepayment penalties on each estimate-if one lender charges a fee for paying off early and another doesn’t, that changes your flexibility. Ask each lender whether their rate is locked or if it floats until closing, since floating rates can increase if market conditions shift.

Negotiate fees and lock in your terms

Request a detailed breakdown of all closing costs and third-party fees, then ask which items are negotiable. Some lenders will reduce origination fees or waive certain charges to win your business. Don’t accept vague language like miscellaneous fees-demand specifics. Once you’ve narrowed your choice to one lender, apply for preapproval rather than prequalification. Preapproval means the lender has verified your income and credit, making your offer stronger when you find a home. The entire preapproval process typically takes minutes to a few days and gives you concrete proof of your buying power before you start house hunting.

Final Thoughts

You now understand the main mortgage types, how to compare costs honestly, and the steps to select financing that fits your life. Fixed-rate mortgages offer predictability, adjustable-rate mortgages can save money if your timeline is short, and government-backed programs like FHA, VA, and USDA loans open doors for buyers who might otherwise struggle to qualify. The key takeaway is simple: interest rates matter far less than your total cost, which includes fees, closing costs, and mortgage insurance.

Comparing options isn’t optional if you want to avoid overpaying. You need at least three loan estimates from different lenders to see real differences in what you’ll actually pay over 15 or 30 years. A rate difference of just 0.5% saves roughly $72,000 on a 30-year loan, but only if you compare APRs and total closing costs across lenders, not just the advertised rate.

Your next move is to gather your financial documents, calculate what you can genuinely afford, and start requesting loan estimates. We at LifeEventGuide help people navigate major life transitions like buying a home by providing clear frameworks and practical checklists-our financing options checklist approach breaks down complex decisions into manageable steps so you can move forward with confidence. Explore our resources to find tools and support for your home buying journey, then apply for preapproval and start your house hunt knowing exactly what you can afford and what you’ll pay.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.