Buying a car is one of the biggest purchases you’ll make, and it’s easy to feel overwhelmed by the options and decisions ahead. We at LifeEventGuide know that having a clear car buying checklist makes the entire process less stressful and helps you avoid costly mistakes.

This guide walks you through each stage, from setting your budget to signing the paperwork, so you can make a confident choice that fits your life and finances.

What Should You Actually Spend on a Car

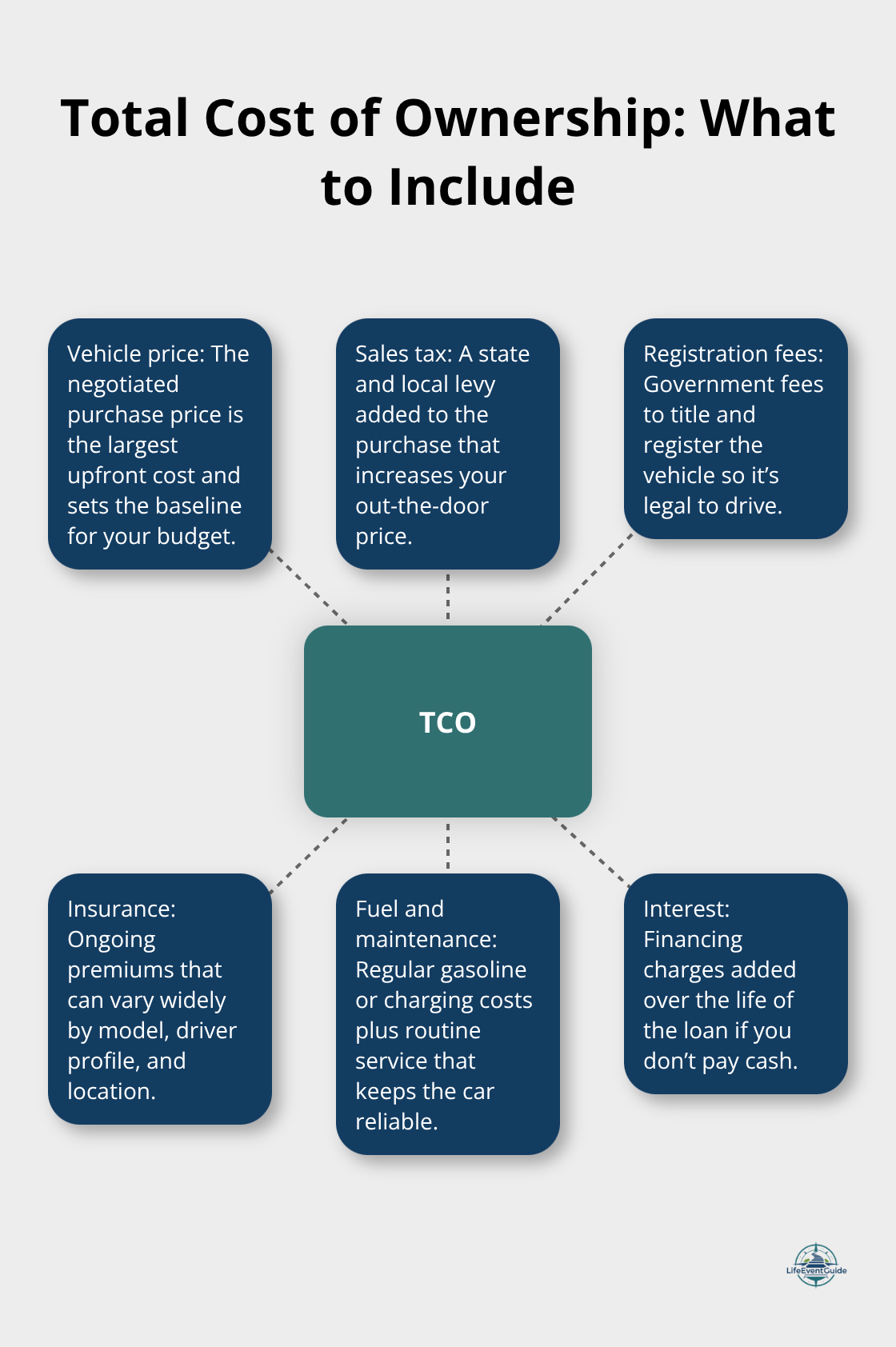

The biggest mistake people make is treating a car purchase like a single transaction instead of a financial commitment that extends years into the future. Your actual cost of ownership includes far more than the sticker price. Calculate your total cost of ownership by adding the vehicle price, sales tax, registration fees, insurance, fuel, and maintenance over the time you’ll own the car. If you finance, factor in interest payments too.

This number often shocks people because it reveals the true financial weight of their decision. Use a car loan calculator to run different scenarios with various down payments and loan terms. The average auto loan in 2025 runs about 69 months according to CNBC, which means you commit to payments for nearly six years. That’s a long time to regret a poor financial choice.

How Much You Can Actually Afford Each Month

Don’t just look at what monthly payment feels comfortable. Instead, follow the 20/3/8 rule: put down 20 percent, finance over no more than 3 years if possible, and keep your total vehicle costs under 8 percent of your gross monthly income. If you earn 5,000 dollars per month, your entire car-related expenses shouldn’t exceed 400 dollars. This includes the monthly payment, insurance, fuel, and maintenance. Most people underestimate insurance costs, so get actual quotes from providers like Allstate, GEICO, Progressive, and State Farm before you fall in love with a specific model. Insurance varies wildly between vehicles and your personal situation.

Your credit score directly affects your financing rate, so check your score at AnnualCreditReport.com before shopping. Scores above 750 typically unlock the best rates, while scores below 650 can cost you thousands in extra interest over the life of the loan. If your score is lower, delay your purchase by several months and work on paying down debt and making on-time payments.

What Your Down Payment Should Actually Be

A 20 percent down payment is the gold standard because it reduces your loan amount, lowers your monthly payment, and protects you if the car depreciates faster than expected. On a 25,000 dollar vehicle, that’s 5,000 dollars down. If you don’t have that saved, consider whether you’re truly ready to purchase. A smaller down payment means higher monthly payments and more interest paid overall.

Secure pre-approval for financing from a bank or credit union before visiting a dealership. This gives you real leverage because you’ll know exactly how much you can borrow and at what rate, which prevents dealers from steering you toward expensive financing options. Compare the dealership’s offer against your pre-approval to verify you’re getting the best deal. With your budget, credit score, and down payment strategy locked in, you’re ready to research the specific vehicles that fit your financial picture and test how the car actually performs on the road.

Research and Compare Your Options

New cars come with warranties, latest technology, and no hidden damage history, but they depreciate in the first year according to Edmunds data, meaning you lose thousands immediately. Used vehicles avoid that cliff, yet you inherit someone else’s maintenance problems and unknown wear patterns. The real question isn’t which is objectively better-it’s which aligns with your budget and risk tolerance. If you have the down payment saved and can afford higher monthly payments, a new car under warranty makes sense. If you’re stretching financially, a used vehicle from 3 to 5 years old often delivers better value because depreciation has stabilized and you can find well-maintained examples with substantial warranty coverage remaining. Certified pre-owned programs from manufacturers typically include extended warranties and thorough inspections, reducing guesswork compared to private sales.

Pull Reliability and Safety Data Before Narrowing Your List

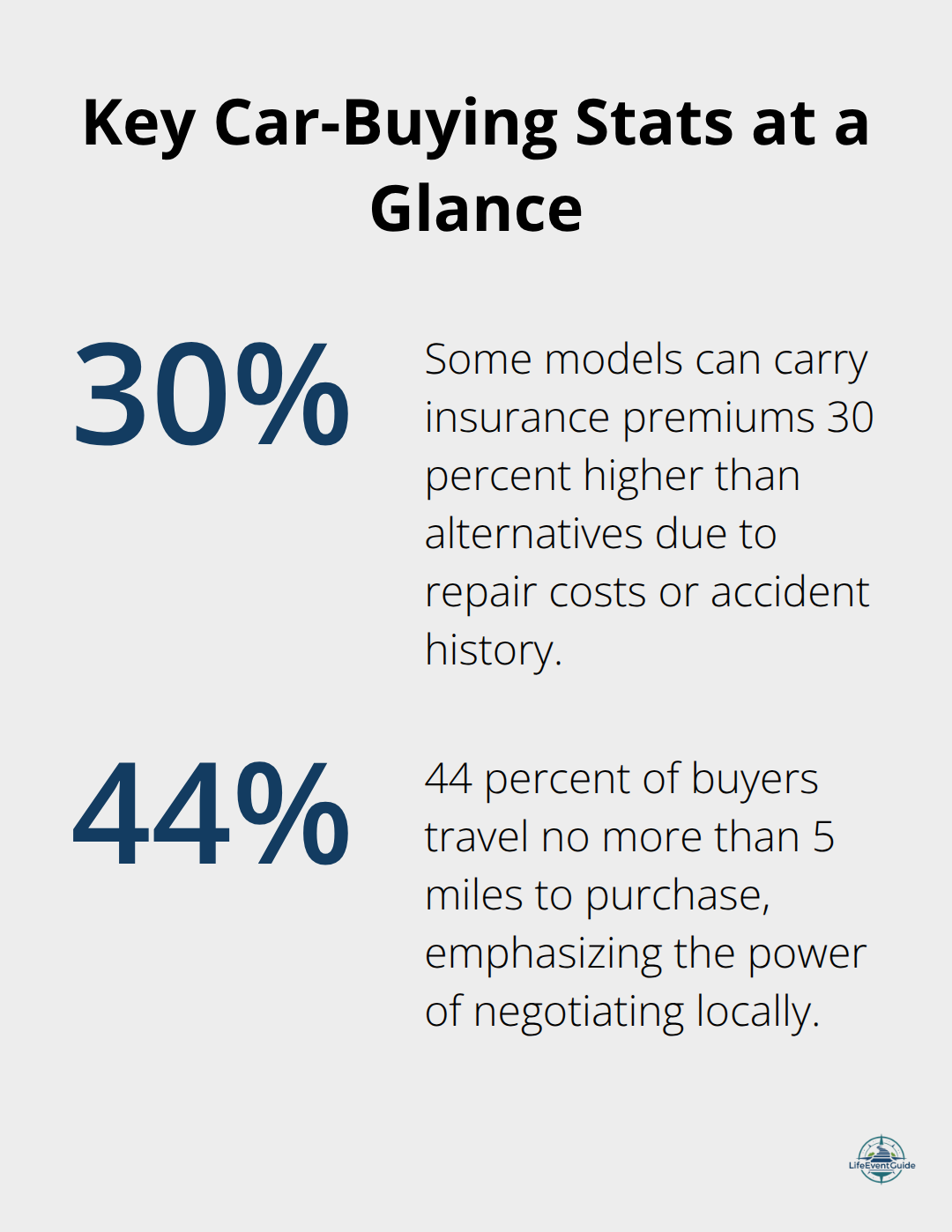

Magazine reviews and manufacturer claims won’t tell you what actually matters. Kelley Blue Book and the National Highway Traffic Safety Administration provide reliability data and safety ratings you can compare side by side for specific models. Insurance quotes for your top three choices reveal hidden costs-a seemingly affordable car might carry premiums 30 percent higher than alternatives due to repair costs or accident history. The EPA estimates on fueleconomy.gov show actual fuel economy rather than manufacturer figures, which often run optimistic.

For used cars, a Carfax or AutoCheck report immediately reveals accidents, title issues, mileage discrepancies, and maintenance records that determine whether a vehicle is reliable or a money pit. A car with consistent oil changes and service records outperforms a lower-mileage vehicle with gaps in maintenance history.

Build Your Shortlist Based on Real Costs and Availability

Three to five models that meet your transportation needs, fit your budget (including insurance and fuel costs), and have strong reliability ratings form your working shortlist. Narrow this further by checking local inventory across dealerships using Autotrader, Cars.com, or CarGurus to understand pricing variations and availability in your area. Regional price differences are substantial-the same 2022 Toyota Camry might cost 22,000 dollars in one state and 19,500 dollars in another depending on supply and demand. Focus on local dealers first since 44 percent of buyers travel no more than 5 miles to purchase, according to Demand Local research, meaning you can negotiate better when you’re nearby and ready to act quickly. With your shortlist finalized and pricing data in hand, you’re prepared to move into the actual buying process where test drives and inspections separate the right vehicle from the wrong one.

How to Lock In the Right Deal

Prepare Your Documentation and Approach

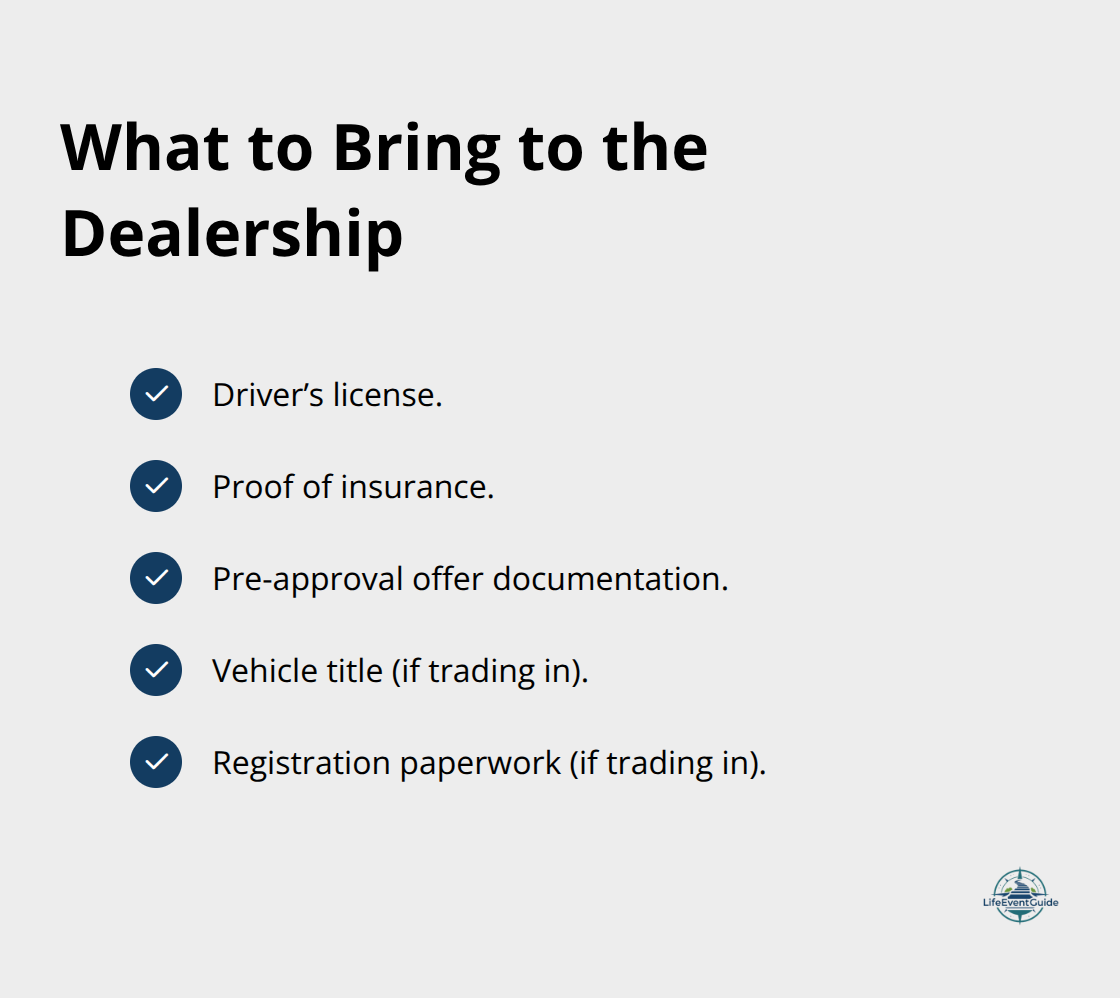

Arrive at the dealership with research, pre-approval, and a shortlist in hand so you act decisively rather than emotionally. Bring your driver’s license, proof of insurance, and documentation of your pre-approval offer to every dealership visit. If you’re trading in a vehicle, gather the title and registration beforehand so paperwork flows smoothly. This preparation eliminates delays and signals to dealers that you’re a serious buyer ready to move forward.

Test Drive and Inspect Thoroughly

The test drive matters far more than most buyers realize. Spend at least 30 minutes on both highway and city streets to assess acceleration, braking, handling, and how all the features actually function in real conditions. A car that feels fine during a 10-minute loop around the dealership often reveals problems during genuine driving. Listen for unusual noises, check blind spots, test the infotainment system, and pay attention to how the vehicle responds to your inputs. Some problems only surface when you’re merging on a highway or navigating tight parking situations.

For any used vehicle, hire an independent mechanic inspection before you commit. This evaluation helps you assess the condition of the car and prevents purchasing a vehicle with hidden mechanical problems that could cost thousands to repair. The inspection report gives you concrete leverage during negotiations because issues become objective facts rather than disagreements about condition.

Negotiate From a Position of Strength

Negotiation starts with knowing your walk-away price before you enter the dealership. Use your pre-approval amount, the vehicle’s Kelley Blue Book value for its specific year and mileage, and any comparable sales data from your local market to anchor a reasonable offer. According to DAS Technology’s Lead Response Study from 2025, dealers who respond to inquiries within five minutes are 21 times more likely to convert sales, which means they’re motivated to move quickly. Use this to your advantage by obtaining multiple quotes and letting dealers know you’re comparing offers.

Start negotiations from a data-backed position rather than the sticker price. Focus on the out-the-door price including taxes and fees rather than monthly payments, and understand your trade-in value separately so you’re not confused during discussions. Never let emotions override your budget or credit score research-the wrong car at a high interest rate will drain your finances for years.

Review and Sign the Final Paperwork

Before signing any paperwork, review every line of the contract and verify that all numbers match your negotiated price. Confirm the vehicle identification number matches your test-drive vehicle, and check that promised warranties or incentives appear in writing. Sign only when everything aligns with your pre-approval terms and your 20/3/8 budget rule still holds true.

Final Thoughts

Before you sign the paperwork, verify that every number on the contract matches your negotiated price and that all promised warranties or incentives appear in writing. Confirm the vehicle identification number matches the car you test-drove, and check that your financing terms align with your pre-approval. Walk away if anything feels rushed or doesn’t match your budget.

The most common mistakes happen when buyers skip steps in their car buying checklist. Skipping the pre-approval leaves you vulnerable to dealer financing that costs thousands more, ignoring insurance quotes means you discover after purchase that your dream car carries premiums you can’t afford, and rushing the inspection or test drive surfaces problems only after you’ve signed. Letting emotions override your 20/3/8 budget rule leads to payments that strain your finances for years.

After you buy, secure your car insurance immediately and review the maintenance schedule in your owner’s manual. Follow the recommended service intervals to protect your investment and maintain reliability. Keep all receipts and service records because they document the vehicle’s condition and support its resale value later, and visit our resources on major purchases to explore how we guide people through life transitions with clarity and confidence.

Publisher’s Note: LifeEventGuide is an independent educational publisher. Some articles reference tools or services we recommend to help readers explore options related to major life transitions. Learn more about how we make recommendations here.